Don’t Get Too High on Potential Marijuana Revenues

Introduction

Recreational marijuana has been legalized for commercial sale and personal consumption in 10 states and Washington, D.C. as of November 2018. Of the states that have legalized recreational marijuana, seven have active commercial markets for sales including a New York State neighbor, Massachusetts. Three more states are finalizing rules and regulations to facilitate sales in the near future including another New York State neighbor, Vermont.

There is growing speculation that Democratic control of the executive and legislative branches coupled with rising public support present the strongest opportunity for recreational marijuana legalization to date. There is potential for new revenue from new and existing taxes that may be imposed on the recreational marijuana industry. Although the new legislature has not yet convened, suggestions already have emerged as to how to spend the hypothetical new revenue, including investing the revenue in mass transit and directing the funding to communities disadvantaged by decades of marijuana law enforcement.1

Advocates, stakeholders, and elected officials must be cautious in these early discussions regarding speculative revenues. Evidence from other states, as well as research conducted by the New York State Department of Health (DOH) and the New York City Comptroller, point toward significant revenue potential from the multibillion dollar marijuana industry. But the evidence and research also reveal that many months or years of careful crafting of legislation, regulation, infrastructure, and market development precede consistent revenues.2

Background on recreational marijuana programs nationally

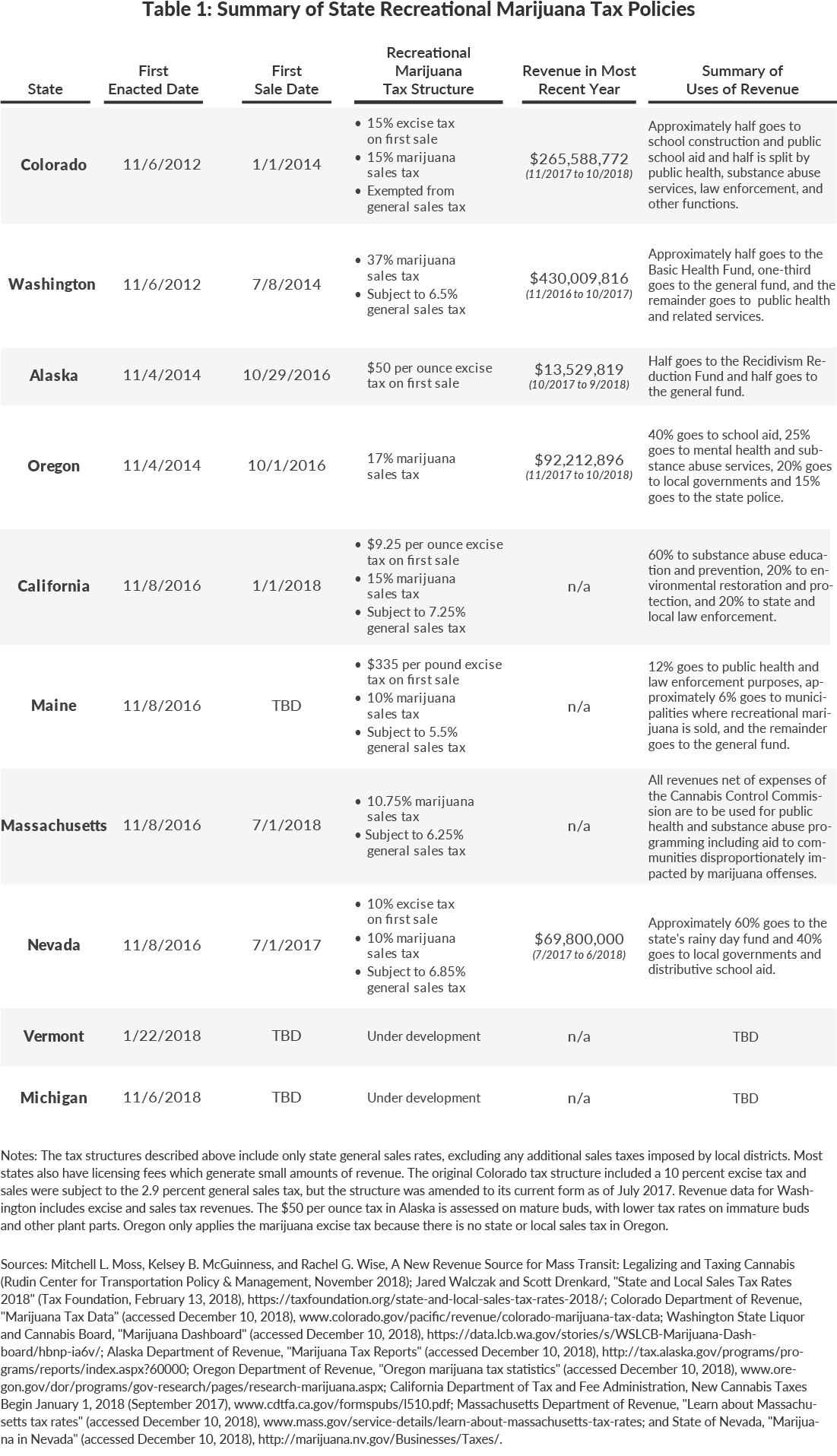

Colorado and Washington were the first states in the nation where voters approved legalization of recreational marijuana in November 2012. Since then eight more states have approved legalization. These states have implemented varying tax structures. Most levy a sales tax; some levy a sales tax and an excise tax; and others levy a sales tax and a higher marijuana sales tax on purchases.3 (See Table 1.) The associated revenues are significant. In Washington State, which levies a 37 percent marijuana sales tax in addition to a 6.5 percent general sales tax, more than $430 million was collected in fiscal year 2017.

While states’ legal markets are starting to realize significant revenue, they experienced major fiscal and programmatic implementation challenges, with issues plaguing production and consumption, which in turn impacted tax revenues:

- Production Issues in Oregon: Growers in Oregon quickly developed production capacity that is several times greater than consumption. This has led to oversupply that has driven prices (and thereby tax revenues) down, caused vast overuse of resources such as water, forced the state to stop accepting new applications for growth sites, and is likely to lead to a market in which large out-of-state conglomerates crowd out developing in-state growers.4

- Consumption Issues in California: California’s legal recreational market has not grown as predicted. Experts have cited a rocky rollout, high taxation, and the entrenched illicit market as reasons California received only $82 million in tax revenue in the first six months of sales, compared to projected revenues of $185 million.5

While other states have not had such fundamental issues with development of the legal recreational market, their experiences show there is still a long delay in receiving tax revenues. Alaska, Oregon, and Colorado have begun to realize robust receipts from marijuana taxes, but only years after they passed and implemented programs. Colorado, the first state to authorize recreational sales, only started to realize consistent tax receipts about 4.5 years after its referendum passed. (See Figure 1.)

Implications for New York State

New York can draw on the experiences of other states in crafting the program, but each state, region, and marijuana market is unique.6 DOH released a study on the issue in July 2018, concluding that the public health costs are low, and legalization could generate nearly $700 million in annual tax revenue.7 With popular opinion and legislative control shifting, it is possible that authorizing legislation will be adopted in 2019.8 Stakeholders, interests, and elected officials are already arguing over how to spend the money when it materializes, but there are reasons to be concerned and cautious about potential revenue:

- Implementation timing: It takes time to pass legislation, write regulations, implement the program, and collect tax revenue. As shown in Table 1, most states took approximately two years between passage and revenue collection in order to develop rules, regulations, and oversight.

- Market timing: It takes time for the market to mature as infrastructure is built by producers and consumers switch from the illicit market to the legal market; this contributed to California missing revenue targets by $100 million in the first six months of sales alone.

- Uncertainty of magnitude: Revenue estimates range widely from $110 million to $428 million for a hypothetical excise tax. New York will need to be more precise.9

- Consumer behavior: Research shows that legalized marijuana reduces alcohol consumption by approximately 12.4 percent.10 In New York this would reduce the State’s alcohol tax revenues by approximately $33 million.

Considerations for appropriate budgeting of new revenue

As New York considers moving forward with legalization, use of revenue should follow these general precepts:

- Caution: Recreational marijuana revenues should not be included in the State financial plan until the very complicated steps of crafting the statute and regulations have been completed; budgeting should not rely upon best guesses or optimistic assumptions. It is better to under-forecast revenues and have a surplus than be overly optimistic and create a deficit.11

- On-budget: Any future revenue should be received and spent on-budget, not through off-budget trusts or other fiscal gimmickry.

- Free from capture: The revenue should not be committed to a specific purpose. Marijuana revenue will be recurring and reliable when the market is mature and should be used for recurring operating budget purposes.12

Conclusion

Potential tax revenue from recreational marijuana legalization in New York State may be significant: it is likely that excise and sales taxes will generate hundreds of millions of dollars in annual revenue. However, early estimates are speculative at best, based on hypothetical tax structures and wide-ranging assumptions of the consumer market. It will take years to fully realize a robust legal recreational marijuana market and associated tax revenue. If New York does implement such a program, the associated revenue must be cautiously forecast, transparently disbursed, and utilized for general state operating purposes.

Footnotes

- Annie McDonough, “Will disadvantaged communities miss out on the marijuana ‘gold rush’?” City & State (October 16, 2018), https://cityandstateny.com/articles/policy/criminal-justice/legalizing-marijuana-gold-rush-racial-disparity.html; and Mitchell L. Moss, Kelsey B. McGuinness, and Rachel G. Wise, A New Revenue Source for Mass Transit: Legalizing and Taxing Cannabis (Rudin Center for Transportation Policy & Management, November 2018), https://wagner.nyu.edu/files/faculty/publications/Report%20-%20Cannabis_and_Mass_Transit.pdf.

- New York State Department of Health, Assessment of the Potential Impact of Regulated Marijuana in New York State (July 2018), www.health.ny.gov/regulations/regulated_marijuana/docs/marijuana_legalization_impact_assessment.pdf; and Office of the New York City Comptroller, Estimated Tax Revenues from Marijuana Legalization in New York (May 2018), https://comptroller.nyc.gov/wp-content/uploads/documents/Legal_Marijuana_051418.pdf.

- Washington, D.C. legalized possession of recreational marijuana. Because it is not a state, is not able to implement a commercial market or impose a tax. See: Mike DeBonis and Aaron C. Davis, "Bowser: Legal pot possession to take effect at midnight in the District," The Washington Post (February 25, 2015), www.washingtonpost.com/local/dc-politics/house-republicans-warn-dc-mayor-not-to-legalize-pot/2015/02/25/2f784a10-bcb0-11e4-bdfa-b8e8f594e6ee_story.html.

- Oregon-Idaho High Intensity Drug Trafficking Area, An Initial Assessment of Cannabis Production, Distribution, and Consumption in Oregon 2018 - An Insight Report First Edition - Updated Version (August 6, 2018), https://static1.squarespace.com/static/579bd717c534a564c72ea7bf/t/5b69d694f950b7f0399c4bfe/1533662876506/An+Initial+Assessment+of+Cannabis+Production+Distribution+and+Consumption+in+Oregon+2018_OR-ID+HIDTA_8-6-18.pdf; and Gillian Flaccus and Kathleen Foody, “Oregon has pot oversupply; Colorado hits the mark,” Denver Post (August 5, 2018), www.denverpost.com/2018/08/05/oregon-colorado-marijuana-supply/.

- Peter Fimrite, “Marijuana Tax Revenue Falls Short in California,” Governing (May 11, 2018), www.governing.com/topics/finance/tns-california-marijuana-taxes-fall-far-short-of-projections.html; and CBS Sacramento, “California Pot Tax Revenue Improves, But It’s Still Far Off Target” (August 15, 2018), https://sacramento.cbslocal.com/2018/08/15/california-pot-tax-revenue-lags/.

- New York State already authorizes prescription of medicinal marijuana. The State’s program was enacted in July 2014 and use began in January 2016. In the period since the program began the State has loosened the original strict regulations on the program to include more conditions eligible for prescription, to allow delivery, and to allow additional practitioners to administer the product. A 7 percent excise tax was placed on all sales of medicinal marijuana. Initial revenue projections of approximately $4 million annually were subsequently revised to approximately $2 million annually. See: New York State Department of Health, Medical Use of Marijuana under the Compassionate Care Act Two-Year Report (November 2018), www.health.ny.gov/regulations/medical_marijuana/docs/two_year_report_2016-2018.pdf; and New York State Division of the Budget, Mid-Year Update to the FY 2019 Enacted Budget Financial Plan (May 2018), p. 81, www.budget.ny.gov/pubs/archive/fy19/enac/fy19myfp.pdf.

- New York State Department of Health, Assessment of the Potential Impact of Regulated Marijuana in New York State (July 2018), www.health.ny.gov/regulations/regulated_marijuana/docs/marijuana_legalization_impact_assessment.pdf.

- Previously introduced legislation to legalize and tax recreational marijuana, the “Marihuana Regulations and Taxation Act,” has not advanced out of committee. The existing proposal would place a per-weight excise tax and a 15 percent marijuana sales tax on legal marijuana, in addition to allowing up to 2 percent additional sales tax option for localities. The legislation proposes distributing 50 percent of funding to a fund for community reinvestment, 25 percent to a drug treatment and education fund, and 25 percent to education after implementation and evaluation expenses are covered. See: S.3040-C/A.3506-C and Will Bredderman, “Cuomo to reveal ‘green new deal’ with marijuana on state’s 2019 agenda,” Crain’s New York Business (December 10, 2018), www.crainsnewyork.com/politics/cuomo-reveal-green-new-deal-marijuana-states-2019-agenda.

- New York State Department of Health, Assessment of the Potential Impact of Regulated Marijuana in New York State (July 2018), p. 19, www.health.ny.gov/regulations/regulated_marijuana/docs/marijuana_legalization_impact_assessment.pdf.

- Michele Baggio, Alberto Chong, and Sungoh Kwon, Marijuana and Alcohol Evidence Using Border Analysis and Retail Sales Data (August 23, 2018), https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3063288.

- Although many states have legalized medicinal and recreational marijuana, neither is recognized by the federal government as legal.

- While it is best to preserve budget flexibility with new revenue sources, most states have chosen to earmark some of the revenues for health programs in recognition of potential social and health impacts that may stem from increased use due to legalization. This would be a reasonable purpose.