New York’s $1 Billion Brownfield Cleanup Program

As New York’s leadership negotiates a final agreement on the state budget for fiscal year 2016, one outstanding issue is the Brownfield Cleanup Program (BCP). Following calls for reform from the State Comptroller, environmental groups, and the 2013 New York State Tax Reform and Fairness Commission, Governor Cuomo proposed stricter eligibility criteria for BCP redevelopment credits in last year’s budget. After the legislature rejected those proposals, the State extended the existing program to December 31, 2015, and the Governor submitted new reforms in his Executive Budget for fiscal year 2016. In their budget resolutions this week, the State Assembly and the State Senate accepted the Governor’s proposed 10-year extension of the BCP, but the Assembly rejected all reforms and the Senate proposed different ones. Further tightening of eligibility, as the Governor has proposed, is important because the program has functioned more as a real estate development program rather than an environmental cleanup program.

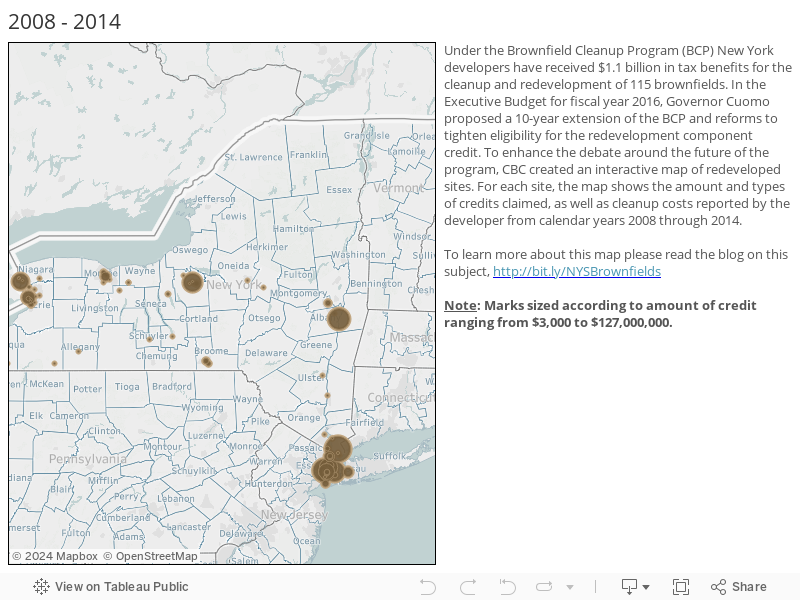

To enhance debate around the future of the BCP, CBC created an interactive map of redeveloped sites in the program. For each site, the map shows total credits claimed, total cleanup costs reported by the developer, and the share of credits for tangible property. The map illustrates the high cost of BCP redevelopment credits and highlights the need to better focus benefits on the cost of cleanup and environmental remediation.

The BCP was established in 2005 to encourage the cleanup and reuse of brownfields – former industrial or commercial properties with significant environmental contamination. The program offers tax credits for site preparation and environmental remediation, as well as redevelopment of the site. From 2008 to 2013, New York issued $1.1 billion in tax breaks to clean up and redevelop 115 sites, an average cost of nearly $10 million per site.1 Although the goal of the program is environmental cleanup, the redevelopment component – called the tangible property tax credit – has accounted for 85 percent of benefits. Notably, the tangible property credit has cost 58 percent more than developers’ cost of site cleanup and groundwater remediation, $963 million versus $609 million, meaning that a 100 percent tax credit for environmental cleanup costs would have been a far more cost effective way to return these sites to productive use.

Benefits have been concentrated in New York City and among large projects. More than half of benefits have gone to New York City projects, and the top 10 projects have accounted for 64 percent of total tax breaks.

Under the Governor’s proposals, eligibility for the tangible property credit would be limited to projects located in high poverty or high unemployment locations (known as “Environmental Zones”), sites where cleanup costs exceed the property value absent contamination, and affordable housing projects.2 The State Senate has proposed applying similar criteria to projects in New York City only. Under the Senate’s proposals, New York City projects eligible for the redevelopment credit would include projects located in Environmental Zones, sites where cleanup costs exceed 33 percent of projected property value absent contamination (rather than 100 percent as proposed by the Governor), affordable housing projects, and projects on underutilized or functionally obsolete sites.3 The Assembly did not propose any changes.

Footnotes

- Reforms adopted in 2008 enhanced cleanup credits and reduced and capped redevelopment credits. If the redevelopment credit caps had been in place for the life of the program, total benefits would have been at least $288 million less. CBC staff analysis of New York State Department of Taxation and Finance, Brownfield Credit Reports, Calendar Years 2008 to 2014, www.tax.ny.gov/research/stats/statistics/special_interest_reports/brownfield_credit/brownfield_credit_reports.htm.

- Environmental Advocates of New York, New York’s Billion-Dollar Brownfields (November 2013), http://f.cl.ly/items/3p3p0f0X2b2O1d3S3h24/brownfields%202013.pdf; New York State Comptroller, Brownfield Restoration in New York State: Program Review and Options (April 2013), pp. 23-28, www.osc.state.ny.us/reports/environmental/brownfields_restoration13.pdf; New York State Tax Reform and Fairness Commission, New York State Business Tax Credits: Analysis and Evaluation (prepared by Marilyn M. Rubin and Donald J. Boyd, November 2013), pp. 62-71, www.capitalnewyork.com/sites/default/files/131115__Incentive_Study_Final_0.pdf; and New York State Tax Reform and Fairness Commission, Final Report (November 2013), p. 25, www.governor.ny.gov/sites/governor.ny.gov/files/archive/assets/documents/greenislandandreportandappendicies.pdf.

- New York State Legislation, S.4209, Part R and A.6009, Part R, www.assembly.state.ny.us/leg/?default_fld=%0D%0A&bn=S04209&term=2015&Summary=Y&Text=Y and www.assembly.state.ny.us/leg/?default_fld=%0D%0A&bn=A06009&term=2015&Summary=Y&Text=Y.