Shrink, Don’t Expand, the New York State Film Tax Credit

The New York State Fiscal Year 2024 Executive Budget proposes to extend and expand the Empire State Film Tax Credit. The State asserts that the proposed changes, designed to compete with other States’ credits, are needed to retain and attract productions to the State and City.

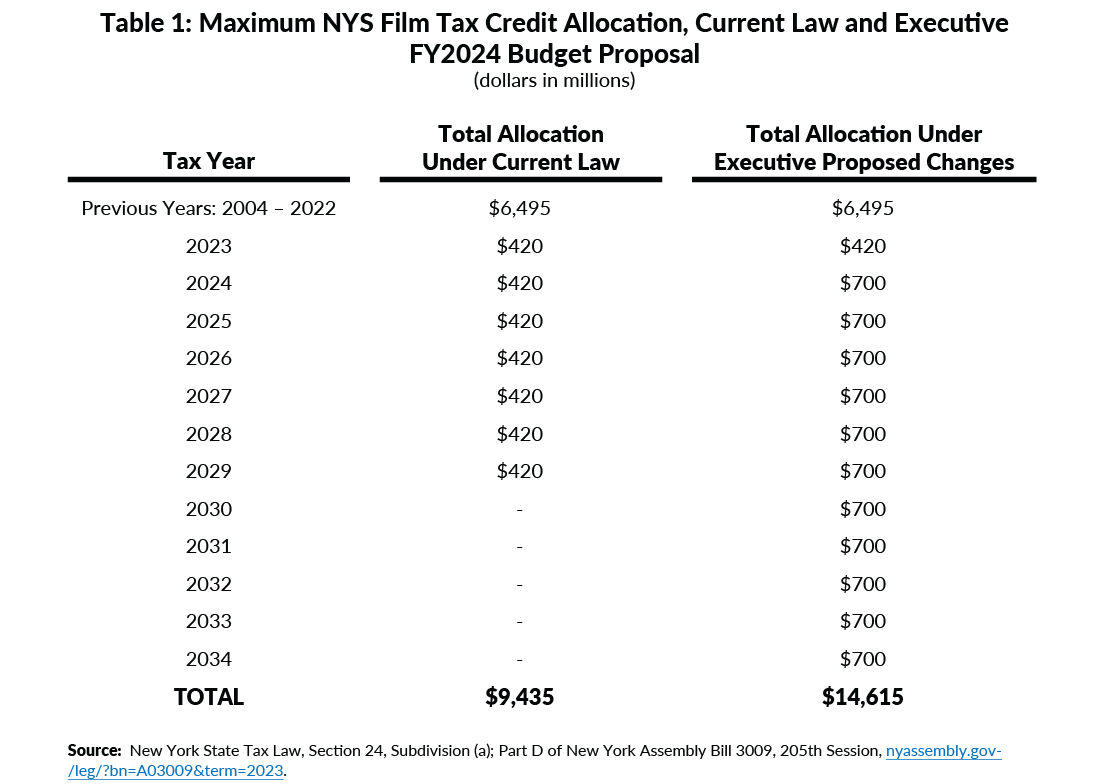

The proposal would increase the annual credit cap from $420 million to $700 million starting in 2024, extend the program’s duration from 2029 to 2034, and increase the value of the credit for beneficiaries; the total maximum cost would increase 55 percent, from $9.4 billion to $14.6 billion.1

Given the current program’s generosity, in the absence of both a rigorous evaluation showing the current credit has produced commensurate economic benefits and analysis demonstrating that the proposed expansion would be economically beneficial, the expansion should be rejected. Furthermore, until such analysis justifies some form of incentive, the State should be shrinking the program.2

The industry has historically located itself in New York to leverage the local pool of specialized labor, facilities, and secondary support industries.3 Despite providing $6.5 billion in credits since the start of the program, the State has not performed a rigorous analysis to show that the program is necessary to attract productions to the State, or whether the foregone tax revenue from the credit exceeds the incremental economic activity of any additional productions attracted.

Furthermore, the credit is already generous and is relatively comparable to other states. New York’s current base rate of 25 percent is higher than California (20 percent) and Georgia (20 percent), but lower than Connecticut (30 percent) and New Jersey (30 percent).4 Increasing the value of the credit for productions is an effort to match or leapfrog other states’ programs. Not only is there no rigorous evidence this is beneficial, but participating potentially needlessly in a back and forth leapfrogging of ever more generous incentives only accelerates a race to the bottom, diminishing revenues instead of competing on New York’s comparative advantage.

The State is now evaluating the efficacy of its economic development incentives. If this evaluation is appropriately rigorous and demonstrates a benefit to preserving some modified version of the current program, it should inform the design of any policy that preserves a film tax credit.5 To demonstrate such a need, the evaluation should determine what economic activity was induced by the incentive, estimate the benefit of that additional economic activity, and compare it to the cost of the program and the impact of using those resources in another manner—the opportunity cost. Furthermore, it should focus on long-run effects, and analytically control for short-term industry fluctuations, especially the impacts of the COVID-19 pandemic.

Roll (Refundable) Credits: How the Film Tax Credit Works

The film tax credit program provides a refundable credit against New York State taxes equal to 25 percent of eligible production costs, such as most of the crew salaries and equipment rental costs, with thresholds for production budgets for both shoots in New York City and outside of the five boroughs.6 The program also provides a relocation credit for large variety shows and a post-production credit for productions shot outside of New York.7 The current program caps annual credits at $420 million, with a maximum of $25 million of that pool going to post-production beneficiaries.

Credits earned in any year that are in excess of the $420 million annual total cap are granted against future year allocations.8 For example, if the 2023 allocation has been fully awarded, the State would issue a credit against the 2024 allocation. As a result, the actual tax expenditure in a given year can exceed $420 million, as taxpayers claim credits granted in prior years. In tax year 2018, the most recent year for which actual costs are available, the film production credit cost $509.5 million and the post-production credit cost $14.8 million.9

Raise the Curtain: Proposal to Extend and Expand the Empire State Film Production Tax Credit

The Executive Budget proposes to increase the annual cap, extend the program, and make the incentive more valuable to individual productions. This would increase the lifetime maximum cost of the program 55 percent, from $9.4 billion under current law to $14.6 billion. (See Table 1.)

The proposal is comprised of two major components. The first component aims to increase the program overall, by boosting the maximum annual total credit cap from $420 million to $700 million beginning in calendar year 2024 while extending the program to 2034, five years beyond its scheduled sunset in 2029.

The second component looks to make the credit broader by increasing the share of a production’s costs that are creditable and expanding eligible expenses, increasing the value of the credit for eligible productions from current levels. The share of costs eligible for a credit would increase from 25 percent to 30 percent for most productions, reversing the decrease from 30 percent of costs enacted in fiscal year 2021.10 Creditable expenses would also be expanded to include the salaries of “above the line” employees, a film industry term for the high-dollar creative leaders on a film project.11 There is no estimate available as to how much the average credit would increase under the proposal, and no evidence provided that this increase would yield economic value for New York.

This broadening also includes changes that would expand the relocation portion of the program aimed at luring existing productions to the state. Eligibility is currently very limited. The proposal modestly expands the eligibility, focusing on a small portion of television production.12 These very specific requirements and eligibility rules suggest the State’s proposal may be targeting specific productions, as has been the case previously.13

Lastly, the Executive Budget proposes increasing the post-production portion of the program from $25 million to $45 million, while also increasing the value of the credit from 30 percent of eligible costs to 35 percent.

Prime Time Competition: State's Credits

Other states’ incentives were cited by the Governor and were a frequent point of discussion by both lawmakers and agency heads at the Joint Budget Hearing on Economic Development on February 9.14 New York’s proposed expansion is intended to match or surpass the film tax credits in other states, including California, New Jersey, and Georgia. The proposed increase to 30 percent of eligible costs exceeds California and matches typical rates seen in New Jersey and Georgia.15 Changes to the relocation credit would provide a credit at a higher rate of 30 percent for two years, surpassing California’s relocation program, which offers a 25 percent credit for one year.16 This competition with other states to attract productions by further subsidizing their costs leads, at some point, to self-defeating competition that drains tax revenues and does not help New York compete on its merits.

Temporary COVID-Related Musical and Theatrical Credit to be Extended and Increased

The New York City Musical and Theatrical Production Tax Credit was created in the Fiscal Year 2021 Enacted Budget to address decreased tourism in New York City and jumpstart the then reopening theatre industry. Currently, the program offers a tax credit for 25 percent of costs, up to $3 million for productions in 2022 and up to $1.5 million for productions in 2023.[17] However, this phase-down is dependent on the New York State Department of Taxation and Finance evaluating the decline of COVID-19 infections and sufficient recovery of tourism to New York City.

The Executive Budget proposes to extend the $3 million production cap to all productions until 2025, remove all phase-down language related to COVID-19, and increase the lifetime aggregate cap for credits from $200 million to $300 million.[18]

The City recently reported that COVID-19 infections have declined, while tourism levels have increased to near pre-pandemic levels.[19] Given these trends, the proposed modifications would transform this COVID-19 response tool to more of an ongoing economic incentive for this industry.

Cut! The Proposed Expansion and Extension Should be Rejected

CBC previously recommended New York phase out this credit, pointing out the State has failed to demonstrate that the credit is necessary to attract productions or create jobs that otherwise would not exist in New York. Biennial evaluations performed by consultants for Empire State Development since 2013 are based on a flawed methodology, which assumes that all productions receiving the credit would not take place in New York absent the credit.20 Some of the productions that receive the credit would have filmed in New York even absent the program. A rigorous evaluation would: determine what economic activity was induced by the incentive, meaning would not have occurred absent the tax credit; estimate the benefit of that additional economic activity; and compare it the cost of the program and the impact of using those resources in another manner—the opportunity cost.

State Law directs the Department of Taxation and Finance to engage a private company to complete a comprehensive assessment of all economic development incentives, including the film tax credit, with a final report due in January 2024.21 Given that the current credit does not expire until 2029, there is ample time to conduct and use that analysis to inform any proposed continuation of the program.

The End: Conclusion

The Empire State Film Tax Credit should not be extended and expanded; absent a rigorous evaluation that demonstrates its need and cost-effectiveness, it should be phased out. New York continues to be a leader among states in economic development incentive program spending, but not in long-term job creation. Tax incentives should only be provided if justified by rigorous analysis. The forthcoming evaluation of State tax incentive programs, which by statute must consider their efficacy, should inform the existence and design of the film tax credit programs instead of actions by other state’s legislatures.

Download Blog

Shrink, Don’t Expand, the New York State Film Tax CreditFootnotes

- Part D of New York Assembly Bill 3009, 205th Session, nyassembly.gov/leg/?bn=A03009&term=2023.

- David Freidfel, Live From New York, It’s Excessive Tax Incentives! (Citizens Budget Commission, October 28, 2020), www.cbcny.org/research/live-new-york-its-excessive-tax-incentives.

- City of New York, Mayor’s Office of Media and Entertainment, New York City Film & Television Industry: Economic Impact Study 2021 (prepared by BuroHappold Cities, Public Works Partners, and Nowhere Office, September 15, 2021), https://www.nyc.gov/assets/mome/pdf/FilmTV_report_091521.pdf.

- For description of state film tax credit programs across the United States, see: Wrapbook, Film Industry Tax Incentives: State-by-State (January 22, 2023), https://www.wrapbook.com/blog/film-industry-tax-incentives; and Jackson Brainerd and Andrea Jimenez, Film Tax Incentives Back in the Spotlight (National Conference of State Legislatures, May 05, 2022, Updated November 17, 2022), https://www.ncsl.org/fiscal/film-tax-incentives-back-in-the-spotlight.

- Review of State tax expenditures is required by Section 180 of Article 8 of the Tax Law of New York State. New York State Department of Taxation and Finance, Request for Proposals 22-100 Economic Impact of New York State Tax Incentive Programs (August 11, 2022), www.tax.ny.gov/pdf/procurement/rfp-22-100-economic-impact-study.docx. Prior evaluations of the film tax credit have not rigorously examined factors such as whether the tax credit attracted productions beyond those that would already select New York State. Prior to any expansion or extension of the credit, rigorous evaluation of this program is needed.

- The film tax credit is predominately a credit against the corporate franchise tax, though a small share is claimed against the personal income tax by unincorporated businesses. For more details, see: David Freidfel, Live From New York, It’s Excessive Tax Incentives! (Citizens Budget Commission, October 28, 2020), www.cbcny.org/research/live-new-york-its-excessive-tax-incentives; and New York State, Empire State Development, “Television and Film,” https://esd.ny.gov/industries/tv-and-film.

- Currently, only variety entertainment, such as a sketch or talk show, in its fifth season with a budget over $30 million and over 200 person studio audience qualify for the relocation portion of the program.

- New York State Empire State Development, Independent Review of the Empire State Film Production and Post Production Tax Credit Programs for 2019 and 2020 (February 24, 2021), esd.ny.gov/esd-media-center/reports/independent-review-empire-state-film-production-and-post-production-credit.

- New York State Department of the Budget and New York State Department of Taxation and Finance, FY 2023 Annual Report on New York State Tax Expenditures (July 21, 2022), www.budget.ny.gov/pubs/archive/fy23/ex/ter/fy23ter.pdf.

- Between fiscal year 2004 and fiscal year 2008, the credit was just 10 percent of eligible expenses. It was then increased to 30 percent. CBC called the decrease from 30 percent to 25 percent a “small step in the right direction should be a first step that begins the credit’s full elimination by decreasing the share of eligible expenses in 5 percentage point increments until it is completely phased-out”. For more details, see: Andrew S. Rein, Recommendations for Legislative Action on the FY2021 NYS Executive Budget, Citizens Budget Commission, (February 24, 2020), www.cbcny.org/advocacy/recommendations-legislative-action-fy2021-nys-executive-budget.

- This new inclusion does attempt to negate high dollar salaries of celebrity actors, directors, and writers by capping the maximum eligible salary at $500,000 and capping these salary costs at 40% of the entire production’s credit.

- Currently, only variety entertainment, such as a sketch or talk show, in its fifth season with a budget over $30 million and over 200-person studio audience qualifies for the relocation credit; the proposal reduces the required number of seasons to two. The proposed changes also expand the program to target streaming platform productions of a 30-minute or plus per episode narrative television series with a per episode budget of over $1 million, that have filmed at least six episodes out the state.

- Deadline, NY State Tax Break Seems Tailored For ‘Tonight Show’s Return To NYC (March 2013), https://deadline.com/2013/03/ny-state-tax-break-seems-tailored-for-tonight-shows-return-to-nyc-459438/.

- Joint Legislative Public Hearing on 2023 Executive Budget Proposal: Topic Economic Development (February 9, 2023), http://www.nysenate.gov/calendar/public-hearings/february-09-2023/joint-legislative-public-hearing-2023-executive-budget;and New York State Department of the Budget, FY 2024 New York State Executive Budget Revenue Article VII Legislation Memorandum In Support (February 1, 2023), www.budget.ny.gov/pubs/archive/fy24/ex/artvii/revenue-memo.pdf.

- All three states offer higher rates for productions filming in certain specific targeted areas of the state. For example in New Jersey’s program, all productions that meet the programs base criteria regarding budget size and location receive a base credit of 30 percent, but can enhanced to 35 percent if shooting in specific counties and/or an additional 2-4 percent if the production meets outlined diversity criteria. Georgia’s base credit is 20 percent, but can be elevated by all projects, regardless of geographic or production budget, to 30 percent by including an embedded Georgia logo on an approved project and a link to ExploreGeorgia.org on the project's landing page; California Film Commission, Program Guidelines: California Film and Television Tax Credit Program 3.0 (January 15, 2023), https://cdn.film.ca.gov/wp-content/uploads/2022/05/3-0-Program-Guidelines.pdf; New Jersey Laws 2019, Chapter 506, Section 1, https://pub.njleg.state.nj.us/Bills/2018/PL19/506_.PDF; and Georgia Administrative Code, Department 560, Chapter 560-7, Subject 560-7-8, Rules 560-7-8-.45 Film Tax Credit, Section 7, https://dor.georgia.gov/document/document/rule-560-7-8-45-film-tax-creditpdf/download.

- California Film Commission, Program Guidelines: California Film and Television Tax Credit Program 3.0 (January 15, 2023), https://cdn.film.ca.gov/wp-content/uploads/2022/05/3-0-Program-Guidelines.pdf.

- New York State Tax Law, Article 1, Section 24-C

- Part I, Subsection E of New York Assembly Bill 3009, 205th Session, nyassembly.gov/leg/?bn=A03009&term=2023.

- New York City Department of Health, Long-Term COVID-19 Trends (Accessed February 9, 2023), www.nyc.gov/site/doh/covid/covid-19-data-totals.page; and NYC & Company, NYC & Company Announces New York City Tourism to Reach 56.4 Million Visitors In 2022 (December 22, 2022), https://business.nycgo.com/press-and-media/press-releases/articles/post/nyc-company-announces-new-york-city-tourism-to-reach-546-million-visitors-in-2022/.

- Empire State Development, Economic Impact of the Film Industry in New York State, 2019 2020, (February 22, 2021), https://esd.ny.gov/esd-media-center/reports/independent-review-empire-state-film-production-and-post-production-credit.

- New York State Tax Law, Chapter 60, Article 8, Section 180, https://www.nysenate.gov/legislation/laws/TAX/180.