Steep Incline and Cliffs Ahead:

Unaffordable NYS FY 2024 Spending Proposals Put Future at Risk

INTRODUCTION

New York State’s budget has recently grown at an incredible and unsustainable rate, risking future instability and setting the stage for damaging service cuts or counterproductive tax increases. This year’s budget proposals by the Governor, Senate, and Assembly not only fail to address the State’s structural budget imbalance, but make it worse.

Without appropriate spending restraint, by fiscal year 2027 the State could face structural deficits of $15 billion under the Governor’s plan or nearly $20 billion if the Legislature’s plans are enacted. While conservative receipt estimates often overstate gaps, the State’s looming problem far exceeds that possibility and coincides with an uncertain economic outlook and continued outmigration. Delaying action to reduce the State’s fiscal imbalance increases the risks of deep cuts, squandering reserves even without a recession, and uncompetitive tax increases.

CBC’s analysis of recent State spending and the current proposals found that:

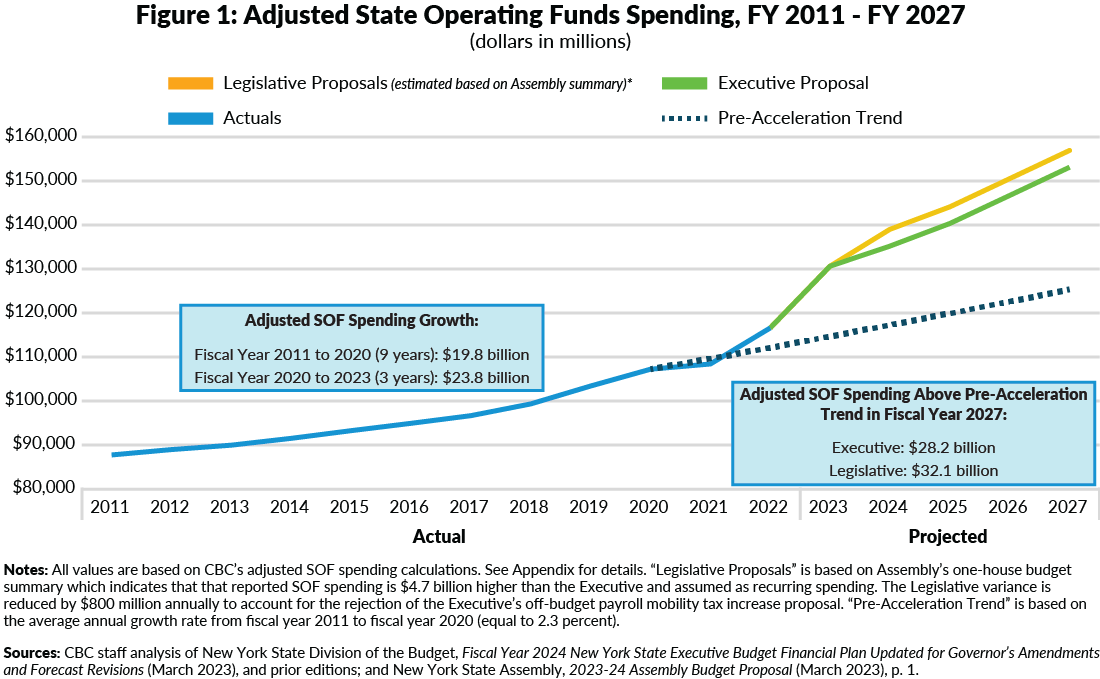

- State Operating Funds (SOF) grew approximately $23.8 billion from fiscal year 2020 to fiscal year 2023, eclipsing growth of $19.8 billion over the prior nine years, when adjusted for timing shifts and spending moved off budget;

- Adjusted SOF spending is slated to increase 12.2 percent between fiscal years 2022 and 2023;

- The Executive Budget proposes to increase spending 3.6 percent in fiscal year 2024 and 4.3 percent annually thereafter, driven by the addition of $2.4 billion in new, recurring spending;

- The Legislature proposes to add $3.9 billion in annual spending to adjusted SOF above the Governor’s proposal;

- Accelerating spending growth opens budget gaps by fiscal year 2027 totaling $7.2 billion under the Governor’s proposal; and

- The State’s structural gap in fiscal year 2027 widens to $15 billion under the Governor’s proposal and nearly $20 billion under the Legislature’s, absent the benefit of billions of dollars in federal fiscal aids, prepayments, and expiring temporary taxes.

To set the State on a path to fiscal stability and security, the State’s Fiscal Year 2024 Enacted Budget should:

- Restrain SOF spending growth to 2 percent annually;

- Allow temporary tax increases to sunset as scheduled (or earlier);

- Maintain or expand the Governor’s Rainy Day reserves plan;

- Publish basic financial plan tables with the enacted budget; and

- Reform the State’s budgeting and fiscal management to improve services, stability, and accountability.

STATE SPENDING GROWTH ACCELERATED DURING THE PANDEMIC; EXECUTIVE AND LEGISLATIVE FISCAL YEAR 2024 PROPOSALS ADD BILLIONS OF DOLLARS MORE

The Governor’s Fiscal Year 2024 Executive Budget proposes to increase SOF spending approximately $3.2 billion. This includes a $2.4 billion reported increase plus $800 million from off-budget spending.1 This new spending is on top of already extraordinarily high SOF spending growth in the last three years. From fiscal year 2020 to fiscal year 2023, adjusted SOF spending is projected to increase approximately $24 billion, eclipsing growth of $20 billion over the prior nine years. (See Figure 1.)

This rapid growth includes a year-over-year increase of 12.2 percent from fiscal year 2022 to fiscal year 2023; under the Governor’s proposal projected growth is 3.6 percent in fiscal year 2024 and 4.3 percent annually thereafter. By any measure, spending growth is exceptionally high; it jumped following the initial pandemic period, and is now slated to grow at more than twice the rate of the preceding nine years (2.3 percent average annually between fiscal years 2011 and 2020).

The Legislature’s proposals would drive spending even higher, adding approximately $3.9 billion in annual spending on top of the Executive proposal. The Assembly’s one-house budget summary identifies $4.7 billion in additional SOF spending, and it rejects $800 million in off-budget spending proposed by the Executive associated with the payroll mobility tax. The new spending is supported in part by approximately $2 billion in new temporary tax increases on businesses and personal income.

PROPOSED SPENDING DRIVES ANNUAL SOF SPENDING OVER $28 BILLION HIGHER THAN THE PRE-ACCELERATION TREND BY FISCAL YEAR 2027

The jump and continued acceleration in spending put the SOF spending trajectory far above the prior trend. The Executive Budget proposal would exceed the prior trend by $28.2 billion by fiscal year 2027; the difference jumps to $32.1 billion with the Legislative proposal. Much of this is due to the State’s decision to ‘fully fund’ education foundation aid without sufficient offsetting savings, and growth in Medicaid.

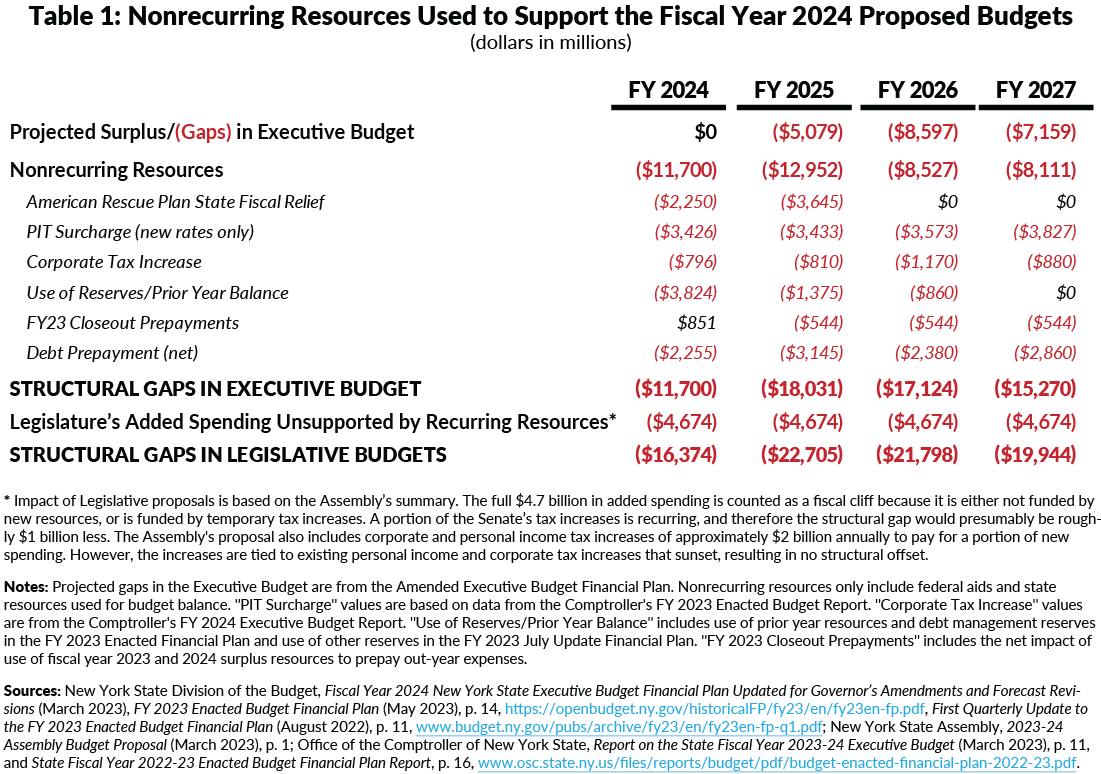

SPENDING DRIVES BUDGET GAPS IN OUT-YEARS; END OF TEMPORARY RESOURCES WIDENS EVEN FURTHER

Proposed spending growth far outstrips receipts growth, even as the Governor, Senate, and Assembly all raise additional receipts through increased taxes on business and personal income (mostly temporary). From fiscal year 2023 to fiscal year 2027, State receipts are projected to grow 1.1 percent on average annually, with average annual increases of 1.9 percent for personal income tax receipts and 0.8 percent for all other taxes.2 At the same time, extraordinary federal aids—including unrestricted fiscal relief and targeted supplemental aids—will be exhausted in the coming years, with total federal aid decreasing $7.8 billion (9 percent) over the same period.3

As a result, the Executive Budget financial plan forecasts annual gaps of $5.1 billion, $8.6 billion, and $7.2 billion in fiscal years 2025, 2026, and 2027, respectively. However, these gaps dramatically understate the State’s fiscal challenges because they are narrowed by billions of dollars in nonrecurring resources including prepayments from prior year surpluses and expiring temporary taxes. The $7.2 billion fiscal year 2027 gap would be much larger if not for receipt of $4.7 billion in sunsetting personal income and business tax increases plus spending lowered by $3.4 billion in prepayments using funds from prior periods. Removing those temporary resources exposes the structural gap totaling $15.3 billion.

Based on the Assembly’s budget summary, the Legislature’s plans—with $4.7 billion in net new recurring spending above the Governor’s proposal—expand that structural imbalance even further.4 Approximately $2 billion in new temporary taxes fund a portion of the $4.7 billion in higher spending. Therefore, Legislative budget gaps are approximately $2.7 billion higher than the Executive in the out-years. Because the major tax increases proposed by the Assembly are temporary, their expiration does contribute to the structural deficit. By fiscal year 2027, the total structural imbalance would reach nearly $20 billion if the Legislature’s plan were enacted.

This year’s Executive Budget proposed extending the business tax increases worth roughly $1 billion annually for another three years, through 2026, an action both one-house budgets accepted. The one-house budgets included further tax increases: matching proposals to raise roughly $1 billion from personal income taxes and varying proposals to raise another $1 billion from additional business tax increases. These proposed increases are extensions or enhancements of the $5 billion annual tax increases enacted two years ago.

Tax increases play a significant role in the structural gaps, both directly and indirectly. Because many of them are temporary, it means that recurring spending is supported by nonrecurring resources (a ‘cliff’). They also exacerbate the problems of the State’s uncompetitive tax environment, which—along with the many other factors that make living and operating a business in the State more expensive—contributes to outmigration and incentivizes businesses and individuals to locate elsewhere.

RECOMMENDATIONS

To stabilize the State’s fiscal health and ability to protect services to New Yorkers, the enacted budget should restrain spending, improve tax and economic competitiveness, and pursue budget and fiscal management reforms. Specifically, the State should:

- Restrain SOF spending growth to 2 percent annually. Restraining SOF spending growth to 2 percent annually would bring spending trends in line with receipts, closing forecast gaps.

- Allow temporary tax increases to sunset as scheduled or earlier. Spending restraint is necessary for the temporary personal income taxes and business taxes to sunset as scheduled. Accelerating the taxes’ expiration would improve New York’s competitiveness, both reducing the costs of living and doing business in New York, and sending a signal to those who may consider coming or leaving. New York already has the nation’s highest top marginal personal income and business rates, when combined with New York City and the Metropolitan Transportation Authority region, risking the State’s attractiveness for residents and business.

- Maintain or expand the Governor’s Rainy Day reserves plan. Last year’s budget agreement included a plan to substantially increase the State’s principal reserves, accumulating more than $19 billion in the Rainy Day Fund and other reserve funds over three years. The Governor this year proposes accelerating that plan to make all deposits this year, and to wisely raise balance and deposit caps on the Rainy Day Fund. These plans should be implemented, and can be further improved by dedicating more funding to the Rainy Day Fund lockbox and automating future reserves deposits.

- Publish basic financial plan tables with the enacted budget. New Yorkers deserve to know the fiscal impacts of their leader’s choices. Both the one-house resolutions and the enacted budget when agreed to should be accompanied by basic financial plan tables that show the budgets’ size, balance, and out-year impacts.

- Reform the State’s budgeting and fiscal management to improve services, stability, and accountability. CBC recently published a comprehensive budget and fiscal management reform plan that presented four strategies and 12 recommendations to improve budget decisions, transparency, fiscal stability, and service quality. It should increase fiscal integrity by standardizing accounting, building reserves, and better managing debt; improve decisions by providing needed information, and adequate time to use it; bolster oversight and accountability by strengthening fiscal monitors; and improve accountability for the money it spends by implementing a comprehensive system to manage State agency performance.

CONCLUSION

The budget proposals put forward by the Governor, Senate, and Assembly range from very to extremely risky. The proposals all add unaffordable spending, increase the State’s out-year and structural gaps, and raise billions of dollars in new taxes despite New York already having some of the nation’s highest taxes and outmigration. Spending restraint is needed to close gaps, allow temporary tax increases to sunset, and stave off the need for massive, painful service cuts in the future.

APPENDIX

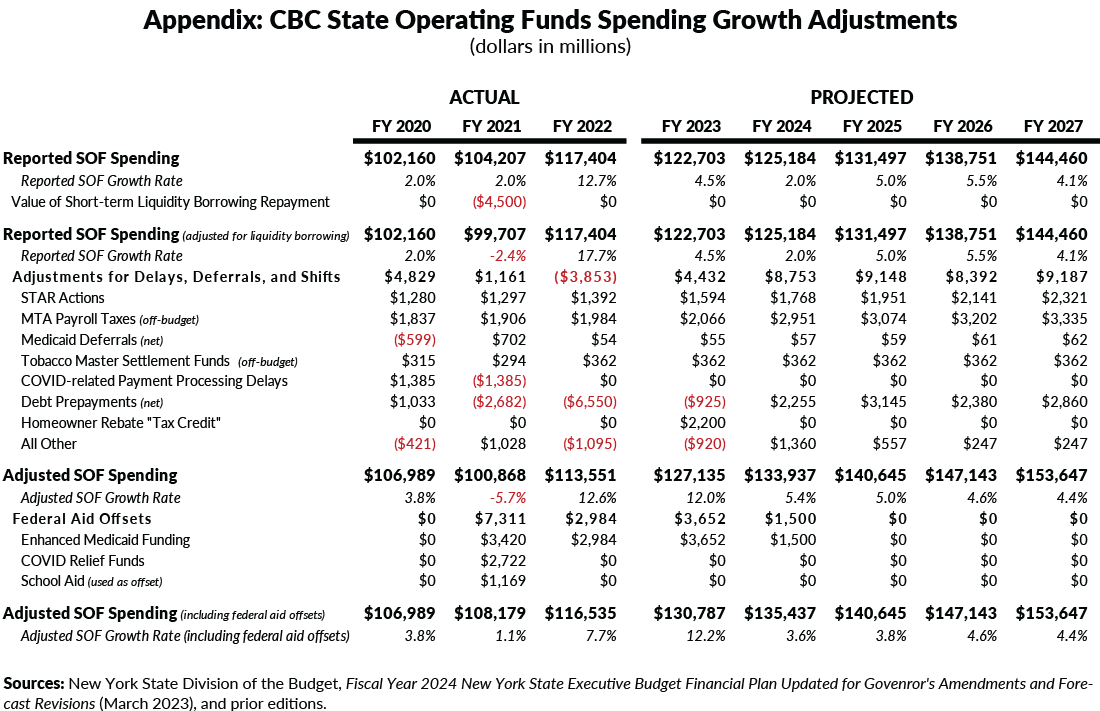

To more accurately and consistently identify spending amounts and trends, CBC adjusts reported SOF spending figures to account for off-budget shifts, payment timing, and other fiscal maneuvers. The State has, over time, used such maneuvers to reduce reported spending or to move payments across years for various reasons. The goal of CBC’s adjustments is to inform more consistent comparisons of year-to-year growth and provide a more complete picture of actual State costs in a given year. This also requires accounting for temporary federal aids that offset State spending, chiefly through enhanced Medicaid funding (eFMAP). The table below summarizes these adjustments. Importantly, while these adjustments generally increase SOF spending totals, they do not necessarily result in adjusted spending growth rates that are higher than reported rates. In fact, CBC’s adjusted SOF spending growth rate for fiscal years 2024 through 2027 is 4.3 percent, less than the 4.7 percent reported by the Division of the Budget.

Footnotes

- Spending added in the Fiscal Year 2024 Amended Executive budget is approximately $2.4 billion to $2.5 billion in fiscal years 2025 to 2027. Approximately $800 million in recurring spending associated with the payroll mobility tax increase is off-budget. See New York State Division of the Budget, Fiscal Year 2024 New York State Executive Budget Financial Plan Updated for Governor’s Amendments and Forecast Revisions (March 2023), p. 17, www.budget.ny.gov/pubs/archive/fy24/ex/fp/fy24fp-ex-amend.pdf.

- Values are based on tax receipts projections in the Fiscal year 2024 Amended Executive Budget Financial Plan, adjusted for the timing of pass-through entity tax impacts. New York State Division of the Budget, Fiscal Year 2024 New York State Executive Budget Financial Plan Updated for Governor’s Amendments and Forecast Revisions (March 2023), www.budget.ny.gov/pubs/archive/fy24/ex/fp/fy24fp-ex-amend.pdf.

- In total, the State Comptroller estimates that the Fiscal Year 2024 Executive Budget relies on $14.9 billion in nonrecurring resources, $10.4 billion of which is extraordinary federal aids that will be exhausted within two years. See Office of the Comptroller of New York State, Report on the State Fiscal Year 2023-24 Executive Budget (March 2023), p. 36, www.osc.state.ny.us/files/reports/budget/pdf/executive-budget-report-2023-24.pdf.

- See New York State Assembly, 2023-24 Assembly Budget Proposal (March 2023), p. 1, www.nyassembly.gov/Reports/WAM/AssemblyBudgetProposal/2023/2023AssemblySummary.pdf.