End the Empire Zones Program and Adopt Excelsior

Last year, New York State began to phase out the roundly criticized program called Empire Zones. The program doles out a panoply of tax incentives to approximately 10,000 firms, either located in an "Empire Zone" or deemed "regionally significant" in return for a commitment to create or retain jobs and to invest capital in the firm's infrastructure. According to the phase-out legislation adopted, no new entrants will be accepted to the program after June 2010; current participants will exit the program as their previously-determined benefit periods end. The first year of the Empire Zones phase-out was estimated to save almost $100 million. The full phase-out will eventually save New York about $600 million annually.

But, if the State Legislature decides to reverse last year's progress by extending the life of the Empire Zones program, New York will be left with a costly program that fails to achieve its aims and an even wider budget gap to fill for the next fiscal year.

Why End Empire Zones?

In 2008, a Citizens Budget Commission examination of the Empire Zones program found three major problems: 1) the original mission of the program to assist economically-depressed areas of the State had been expanded and adulterated over time; 2) a mix of state and local administration had compromised transparency and accountability; and 3) a significant portion of participating firms had not met their targets for job creation and capital investment. In four of New York's 10 regions, more firms in the Empire Zones program failed to meet their jobs and capital investment targets than were successful.

The phase-out of this ineffective program will be a huge win for New York taxpayers. The State Legislature should not extend this program for any period of time, even just another year. Instead, it should adopt new programs that are designed to help develop the State's economy.

Excelsior: Potential for a Better, More Effective Program

A successful economic development program adheres to four criteria: 1) benefits are targeted to industries deemed economically important to the State or local region; 2) benefits are temporary and a bridge to self-sustaining profitability; 3) benefits are allocated based on pre-determined criteria and not to satisfy geographic or political parity; and 4) benefits are calculated according to outcomes in the form of increases in private sector investment. The Excelsior program, a new program proposed by the Governor as part of the Executive Budget, meets these criteria. Tax incentives under the program include a research and development credit, a jobs incentive credit and an investment credit.

- Targeting by Sector and for High Growth: The Excelsior program will provide tax incentives to firms in the fields of high-technology, manufacturing and financial services that agree to add at least 50 jobs in the State. There are valid reasons for targeting these industries.

- The field of high-technology, including clean-tech, bioscience and nano-technology, is expanding rapidly throughout the country. The Pew Center on the States calculates that nationally between 1998 and 2007 the number of clean-tech jobs grew 9.1 percent as total employment grew just 3.7 percent. The current mix of federal policy support and consumer-driven demand for renewable energy and other new technologies suggests that these industries will continue to grow. Other states are already aggressively courting these jobs; New York should do the same to remain competitive.

- Preserving manufacturing is important to retaining large employers with relatively high-wage jobs in many parts of upstate New York. In the North Country, a job in manufacturing pays almost 33 percent more than the average job in the region, yet these jobs are disappearing quickly.

- The financial services industry is vital to the New York City metropolitan area. In 2008, jobs in finance and insurance comprised 9 percent of employment in the New York City, yet equaled fully 32 percent of total wages. And these numbers were generated during a finance-led recession. According to the State Comptroller, financial services employment accounts for about 20 percent of the State's tax receipts. Consequently, through the booms and busts, the health of this sector is intrinsically linked to the fiscal health of New York State.

- The relatively high bar of 50 new jobs will ensure that benefits only go to companies that either relocate to New York entirely from another state or commit to a significant expansion within New York. Either way, Excelsior benefits will be reserved for firms making a long-term commitment in industries essential to the New York economy.

- Toward Self-Sustaining Profitability: Consistent with the second principle of smart economic development, benefit periods and costs under Excelsior are limited. A firm will be eligible to receive credits for five years, and the State will cap its total allocation of new credits at $50 million annually. Applications will be evaluated on a competitive basis because - unlike in Empire Zones - the credits available under Excelsior are not "as of right"

- Pre-determined Criteria to Award Benefits: Empire State Development will select the best applicants according to defined criteria for admission to the program. These criteria will be developed and promulgated through regulations. Benefits will be calibrated so that higher wage jobs will receive bigger tax breaks.

- Benefits Based on Actual Performance: All tax credits will be awarded retroactively based on the prior year's performance. Retrospective audits and attempts to recapture benefits from struggling firms that cannot afford or do not want to return their already-pocketed tax credits will not be necessary.

The Governor's Executive Budget also includes some smaller programs that will address some of the barriers to high-tech, small business and entrepreneurial activity in New York, such as a $25 million New Technology Seed Fund and a $25 million Small Business Revolving Loan Fund. The Seed Fund will invest in startup and early-stage small businesses that have developed new technology products with high potential for commercialization, but have limited access to traditional sources of capital. The revolving loan fund will make low-interest loans to small businesses with 100 or fewer employees. Loans can be used for working capital, debt refinancing, the acquisition of real property, or the acquisition of machinery and equipment. These initiatives also deserve support.

More to be Done

While Excelsior and the smaller programs proposed by the Governor embody sound economic development principles and should be adopted by the Legislature, additional programs and strategic direction are needed to revitalize the State’s economy and set New York on a path for long-term economic growth throughout its regions. Several weaknesses in New York's ability to attract, expand and retain jobs in the so-called "innovation economy" need to be addressed. Recent studies documenting these issues include reports by the Industry-Higher Education Task Force, the Center for an Urban Future, and the Business Council of New York State. These studies reached similar conclusions:

New York lacks a fully functioning innovation ecosystem, defined as a collaborative partnership between business, government, academia and the investment community.

New York's academic institutions focus more on producing revenue from patents and royalties than on working with industry partners to develop new businesses from nascent technologies.

New York places too little emphasis on new business creation and entrepreneurial activity, including financial and professional assistance for early-stage companies developing from technology maturity to profitability.

To illustrate some of New York's shortcomings in this area the CBC compared innovation economy metrics for eight other states identified as New York's competitors. The findings demonstrate that New York falls well below competitor states in key areas essential to building an innovation economy.

Compared to other states, New York lacks a competitive level of research and development undertaken and financed by private business. In 2007, New York industry funded $10.9 billion in R&D, compared to $64.2 billion in California. Moreover, the amount of industry-funded R&D increased 6 percent in New York from 1998 to 2007, while all other competitor states increased R&D at an average rate of 83 percent.

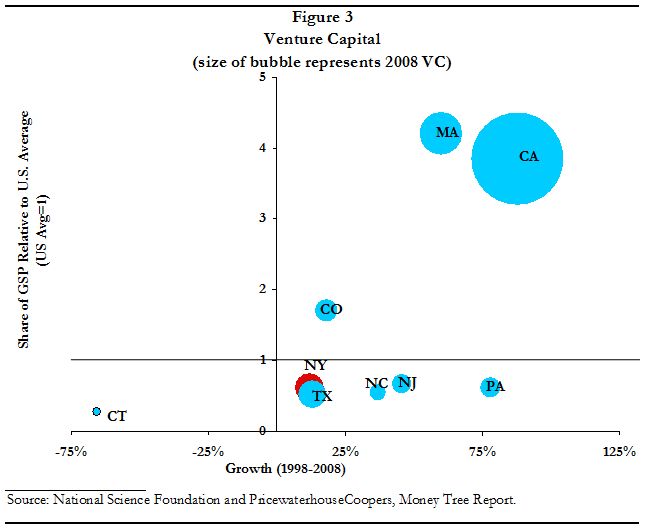

New York also receives a minimal amount of venture capital for new start-ups, despite New York City's standing as the nation's financial capital. In 2008, California companies received $14 billion in venture capital, Massachusetts received $3 billion, and New York received a much lower $1.4 billion. (See Figure 3.) In regard to high-tech venture capital, California received 44 percent of all venture capital distributed nationwide for biotech and Massachusetts received another 21 percent of biotech venture capital. Even New Jersey obtains more venture capital for biotech than New York, $259 million versus $98 million.

A lack of venture capital firms and financial resources is not the problem in New York - New York venture capital firms send $1 billion to California start-ups, while California firms send $160 million to New York start-ups. The lack of venture capital coming into New York and the lack of industry-financed research and development curtail New York's ability to leverage its high level of intellectual capital into new economic opportunities for its residents.

New York's competitor states have created more specific programs on a larger scale to lure high-tech start-ups. Pennsylvania's Keystone Innovation Zones (KIZ), one such example, provides a model. In order to qualify for KIZ designation, a partnership must be established that includes an institution of higher education and a combination of the following types of entities: economic development organizations, private sector businesses, business support organizations, commercial lending institutions, venture capital, and foundations. New companies located in a KIZ may claim a credit equal to 50 percent of their annual growth in gross revenues. In addition, Pennsylvania's Ben Franklin Technology Partners (BFTP) invests alongside angel investors in technology-driven enterprises in sectors such as information technology, life sciences, communications, advanced manufacturing, advanced materials and environmental technology. The Fund makes seed, early-stage, and growth capital investments ranging from $100,000 to $500,000 and provides a direct guarantee of up to 25 percent of the investment made by investors.

New Jersey has also aggressively pursued high-tech. The New Jersey Edison Innovation Zones, in Camden, Newark and New Brunswick, connect state universities, research institutions and related businesses to encourage collaboration and the transfer of scientific research to business. Enhanced financial incentives and lab space are available to eligible technology and life sciences businesses locating in the Zones. New Jersey also offers a host of assistance programs to high-tech companies, including the option to transfer net operating losses to profitable companies, low-cost financing and grants for capital investment at different stages of development, fellowships for doctoral students, and incubator space for emerging technology businesses.

As the name suggests, Excelsior will move New York onward and upward from the failed history of Empire Zones. The program will be more effective and should be put in place as the Empire Zones program sunsets. Ultimately, however, what the State needs is a full strategic plan for economic development that comprehensively addresses barriers and identifies a fuller set of tools to address them. New policies to spur collaboration, change attitudes and build a solid foundation for the growth of new technologies and the jobs that come with them are the key to moving ahead.

By Elizabeth Lynam and Tammy Pels