Options to Enhance the Coordination of Care for Dually Eligible Individuals in New York State

A Discussion Paper

New York State’s Medicaid program, which serves 6 million residents at a cost of more than $70 billion annually, has been undergoing a complex redesign over the past seven years under the Medicaid Redesign Team (MRT). The goal has been to promote the “triple aim” of improving access, enhancing quality, and reducing cost. Key strategies have been expanding managed care services to a growing population and reforming delivery systems. A 2016 report by the Citizens Budget Commission (CBC) found these efforts successful in increasing enrollment, lowering per enrollee costs, and promoting better outcomes for those served.[1]

However, some elements of the redesign plan have faced implementation challenges. CBC, with support from the New York Community Trust, has been exploring options for improving these troubled initiatives. In November 2017 a discussion paper, Challenges of Enhancing Effective Engagement of Community Based Organizations in Performing Provider Systems, released at a forum featuring key stakeholders, identified options to facilitate engaging community partners to improve health care and address social determinants of health through the Delivery System Reform Incentive Payment (DSRIP) program.[2] In May 2018 another discussion paper and forum, Options for Enhancing New York’s Health Home Initiative, addressed the enrollment and performance issues associated with the care management initiative for Medicaid enrollees with chronic conditions known as Health Homes.[3]

This discussion paper focuses on a third element of Medicaid redesign that has faced serious obstacles–the enhanced coordination of care for the 880,000 people enrolled in both Medicaid and Medicare programs. An innovative initiative launched by the MRT was participation in a federal demonstration program to integrate the two programs through a single managed care plan providing both programs’ benefits in coordinated fashion. The new entities, identified as Fully Integrated Dual Advantage (FIDA) plans, were intended to serve two distinct subgroups of the dually enrolled population–those with developmental disabilities and those requiring substantial long-term care services. Both initiatives encountered delays in their design stage and failed to reach their initial enrollment targets.

The initiative aimed at those with developmental disabilities has been revised and extended and is being coordinated with other efforts by the New York State Office for People with Developmental Disabilities (OPWDD) to improve care for that population. Enrollment in this FIDA plan is targeted to a subset of approximately 10,000 individuals with developmental disabilities (I/DD); others in this population will receive enhanced coordination through other mechanisms including specially designed health homes.[4] The latest plan appears to be on a promising track, and as such, this paper does not address additional options for this population.[5]

The FIDA initiative for those with long-term care needs has a particularly problematic history. After negotiations between State and federal officials, the demonstration program was launched in January 2015. Although 22 FIDA plans initially agreed to participate and seek enrollees, enrollment in the first year was disappointing. Significant revisions to the plan were made in December 2015 in an effort to stimulate enrollment and provider participation, but weak enrollment continued to plague the initiative.[6] In early 2019 only 10 plans continued to participate, and enrollment fell below 4,000 out of an initial target population of about 110,000.[7]

This paper focuses on options to the current FIDA demonstration, which expires at the end of 2019 and may not be extended. It considers enhancements to the demonstration model and alternatives for serving those with long-term care needs and also identifies options to reach dual enrollees with other needs who could benefit from greater care coordination. The paper is organized in three sections: The first provides background information on the nature of the dually enrolled population in New York State; the second describes alternative care coordination arrangements available to serve this population; and the third identifies future strategies for using available mechanisms to improve care coordination for the dually enrolled.

Background

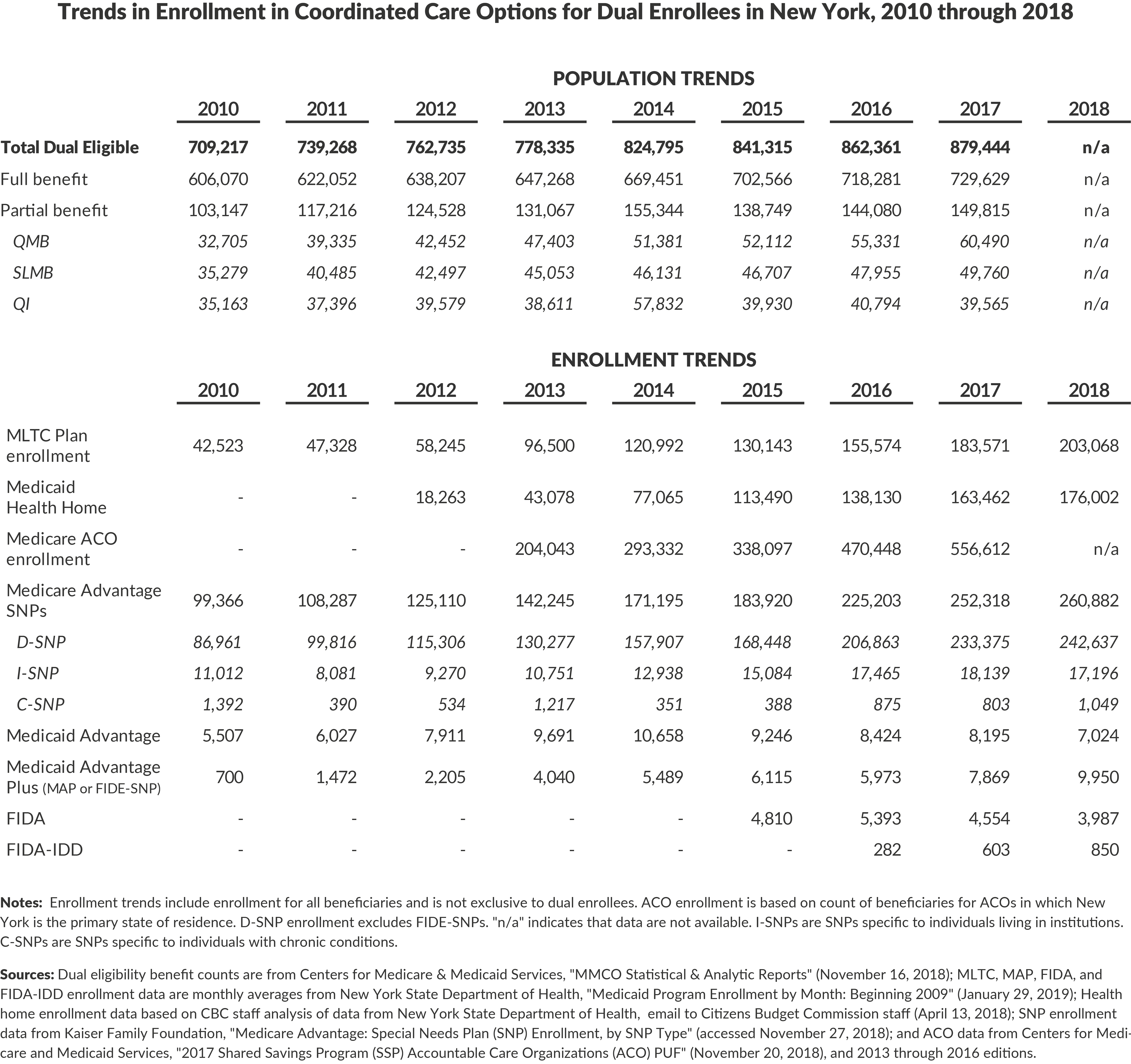

As shown in Figure 1, the number of dually enrolled persons in New York State increased 28 percent from 2009 to 2018 to reach more than 880,000 in the later year. The growth was more rapid than that of the Medicare-only population, and in 2018 the dually enrolled comprised one-quarter of the statewide Medicare population. In contrast the Medicaid-only population grew more rapidly, primarily due to eligibility expansion in the Medicaid program. Currently, the dually enrolled comprise 15 percent of New York’s Medicaid population, but 36 percent of the program’s costs.8

Medicare and Medicaid have different eligibility requirements and different benefits. Dually eligible individuals must meet both sets of eligibility requirements; their benefits are those of the Medicare programs plus supplemental benefits provided by Medicaid.

Medicare Eligibility and Benefits

Medicare eligibility is based on age and disability. Most U.S. residents age 65 and older are eligible; persons under age 65 who have a permanent disability or permanent kidney failure also qualify.9 Qualifying disabilities include a range of physical conditions and mental disorders.

Nationally 89 percent of all Medicare-only enrollees are over age 65, and only about 11 percent qualify due to disability; however, among dually enrolled enrollees greater than 40 percent qualify due to a permanent disability.10 The age and disability characteristics of Medicare-only and dual enrollees in New York State are not reported publicly but likely follow the national pattern of a relatively large share of dual enrollees having a permanent disability.

Medicare benefits are organized into four parts, identified as Parts A, B, C and D. Part A benefits are most inpatient and ancillary services provided by hospitals, some home health services, and post-acute care provided by nursing homes. Part B benefits are hospital outpatient services, physician services, and durable medical equipment. Part D benefits are prescription drugs. Part A and B benefits are paid to providers on a fee-for-service basis by the federal government. Part D benefits are provided by private pharmacy benefit plans selected by the beneficiary from a range of federally approved plans.

Part C is a voluntary option that combines the benefits of Parts A, B, and D. Part C benefits are provided by private insurance plans, known as Advantage plans, which cover and coordinate the services. Advantage plans may also offer supplementary benefits not covered under Parts A and B, and can have lower cost-sharing levels for the enrollee compared to traditional Medicare. However, Advantage plans generally include a narrower choice of physician and hospital providers than is the case for traditional Medicare. Nationally 36 percent of all Medicare beneficiaries have opted to rely on Advantage plans; in New York State the share is 41 percent.11

Medicare benefits require payments from the enrolled individual that include premiums, deductibles, and copayments (fixed dollar amounts per service). Part A has no premium; Part B requires monthly premiums that vary by an individual’s income and in 2018 were $134 ($1,608 annually) for those in the lowest income group; Part D premiums vary with the individual plan averaging about $30 monthly ($360 annually).12 Part C Advantage plans require a premium that varies with the plan; it may be less than the combined premiums for Part B and D benefits or, if greater, may offer other offsetting benefits.

Medicare benefits have deductibles and other out-of-pocket expenses consisting of copayments and coinsurance (a percentage of the charge paid by the individual). The deductible in 2018 for Part B was $183 annually, for Part A it was $1,340 annually for hospital care, and deductibles for Parts C and D varied with the plans offered. Copayments and coinsurance vary by service with the most common charge being a 20 percent coinsurance for many Part B services, but some preventive and other services have no copayment or coinsurance.

An important implication of the Medicare benefit structure is that without Medicaid or other supplementary coverage, Medicare beneficiaries would face substantial out-of-pocket costs for medical care. Annual premiums for Parts B and D (or Part C) approach $2,000 annually. Furthermore, typical Part B deductibles and coinsurance cost hundreds of dollars—a short hospitalization could add more than $1,000, and a serious illness involving a long hospitalization and subsequent nursing home care could lead to a bill of thousands of dollars more.

Medicaid Eligibility and Benefits

Medicaid is a joint federal and state program; the two entities share the costs with the federal government setting minimum benefit and eligibility standards and the states administering the program and having some flexibility with respect to benefits and eligibility. Medicaid is a means-tested program, meaning eligibility depends on one’s income and–for a subset of the Medicaid population–assets. In New York the respective income limits for Medicare-eligible individuals and couples are $859 monthly ($10,300 annually) and $1,267 monthly ($15,200 annually). Asset limits are $15,450 and $22,800 with certain assets such as homes excluded.13 New Yorkers with income higher than the eligibility level may qualify for Medicaid coverage through the “spenddown.” In this case, an individual qualifies for Medicaid when their income less the amount of their medical expenses falls below the Medicaid eligibility level. When the spenddown is met, Medicaid will cover additional health care costs.14

Medicaid benefits include many services also covered by Medicare, notably physician services, hospital care, and limited long-term care services. When both programs cover a service, Medicare is the primary payer, and the state Medicaid program will not cover benefits eligible for Medicare payments.

The advantages of Medicaid coverage for those enrolled in Medicare are twofold. First, Medicaid will pay the premiums and out-of-pocket expenses related to services covered by Medicare. As noted above, this can be a substantial annual sum. Second, Medicaid covers some services not covered by Medicare. The most important of these are for beneficiaries who require long-term care supports and services; these services include long-term nursing home care, personal care at home, and other community based long-term care services. For those requiring these services, the costs can be quite high, and Medicaid provides substantial financial relief.

The federal Medicare Savings Programs (MSPs) are mandates on states to provide partial Medicaid benefits to designated Medicare enrollees who otherwise would not qualify for the state’s Medicaid program. The Qualified Medicare Beneficiary (QMB) program requires states to pay the Medicare premium, copayment, and coinsurance amounts for Medicare enrollees with incomes below 100 percent of the federal poverty level.15 New York’s income limits for full Medicaid benefits are somewhat below that level, so the mandate qualifies some Medicare enrollees for these partial Medicaid benefits. However, since the state income limits are close to the mandated income limits, the spenddown provision likely impacts many of these enrollees, and they may also qualify for full Medicaid benefits. The federal MSPs also mandate that states pay the Medicare Part B premium (but not copayment and coinsurance) for Medicare enrollees with incomes between 100 percent and 135 percent of the federal poverty level. Those with incomes between 100 percent and 120 percent of the poverty level are designated Specified Low-Income Medicare Beneficiaries (SLMB), and their premium is financed jointly by the state and federal governments like other Medicaid benefits; those between 120 and 135 percent of the poverty level are designated Qualifying Individuals (QI), and their premium is funded fully by the federal government.

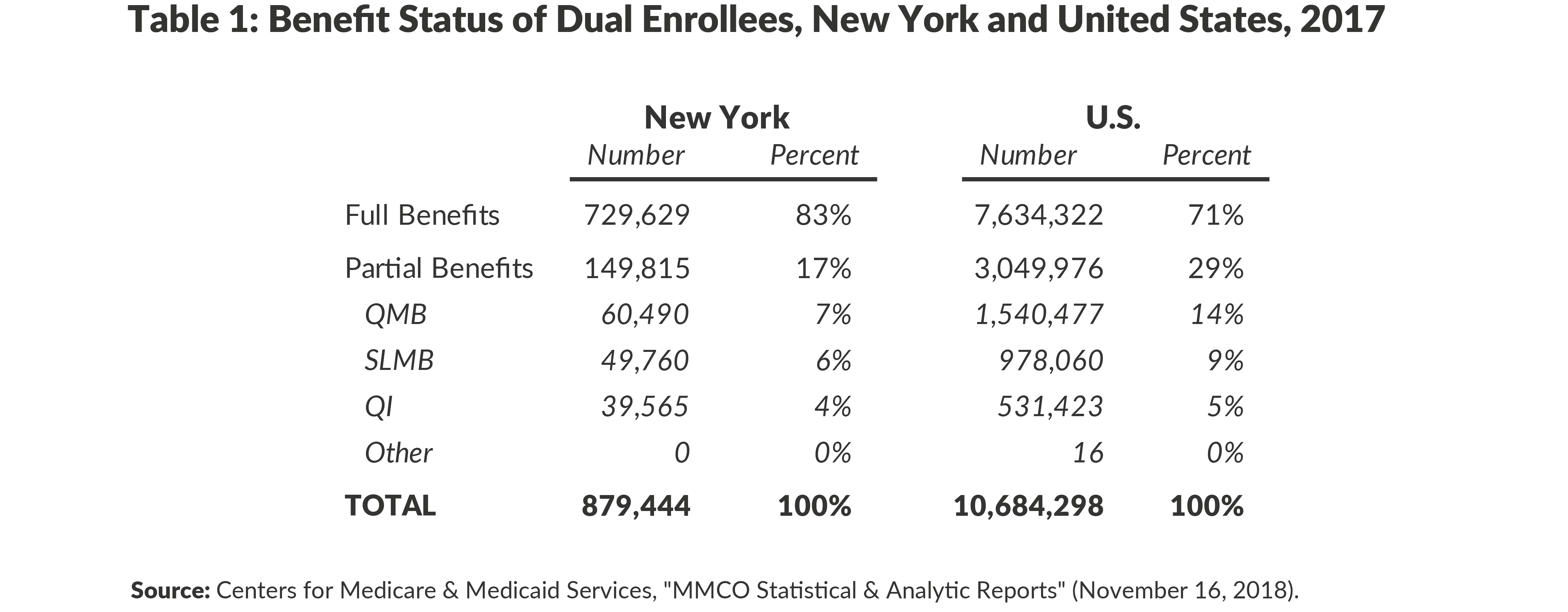

As shown in Table 1, about 17 percent of the dual enrollees in New York qualify only for partial benefits, a smaller share than nationally (29 percent). Most of the difference is related to the smaller share in the QMB program in New York (7 percent versus 14 percent); as noted earlier this likely is due to the ability of many individuals with incomes below the poverty level to qualify for full Medicaid benefits under New York’s income eligibility rules.

Characteristics of the Dual Enrollee Population

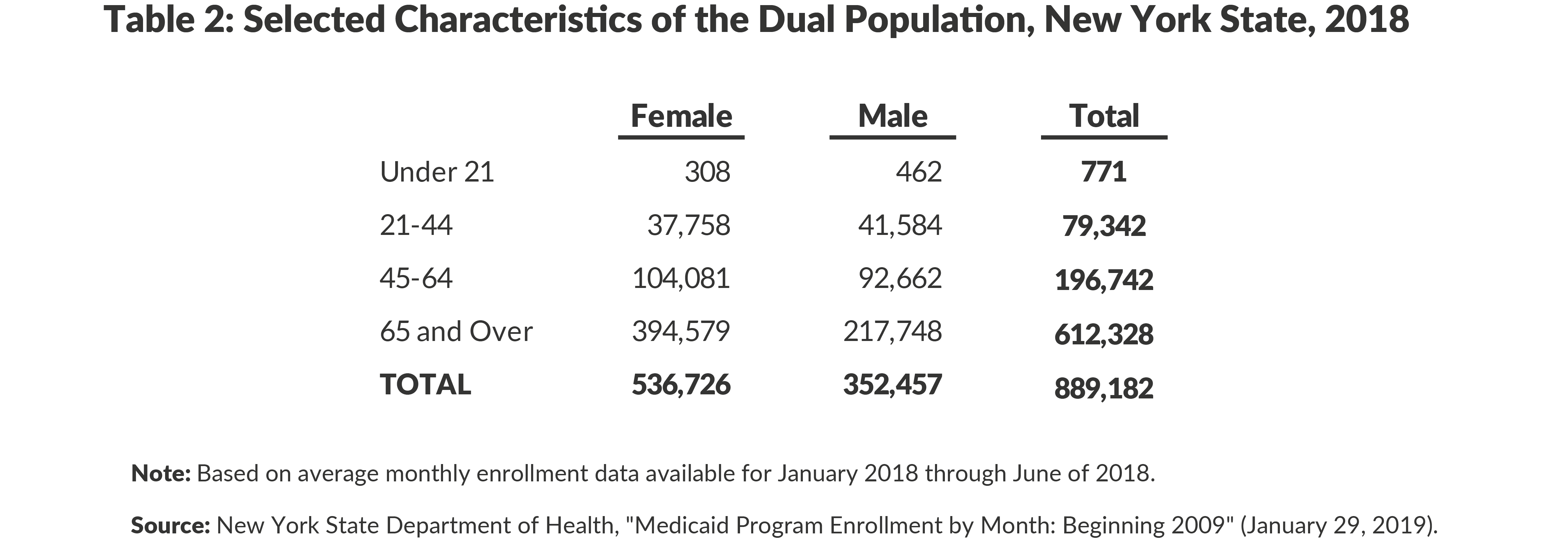

Tables 2 and 3 summarize the limited data available relating to the characteristics of New York’s dual enrollee population. As noted, about 69 percent are over age 65, and 31 percent are younger with a disability. About 60 percent are female, with a somewhat higher female share among those older than age 65 (65 percent) and a somewhat smaller share of females among the younger disabled group (51 percent).

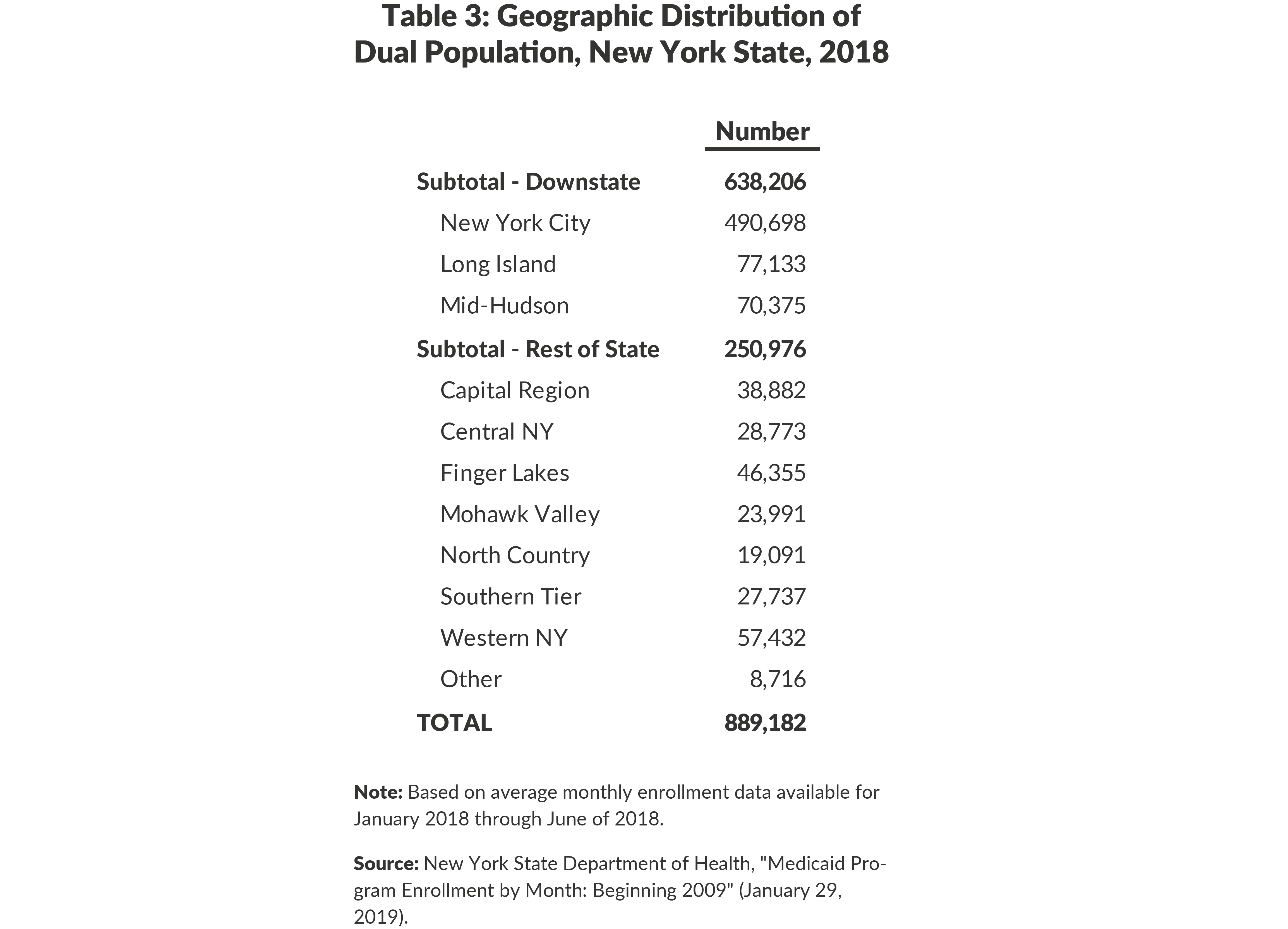

A majority (55 percent) of the dually enrolled population lives in New York City. Including the Mid-Hudson area and Long Island brings the downstate share of the dually enrolled population to 72 percent.

Data relating to the health status and medical care utilization of the dually enrolled population are available only from a few national studies. Compared to non-dual eligible Medicare enrollees, the dually eligible group is more likely to have three or more chronic conditions (72 percent versus 65 percent) and to have a cognitive or mental impairment (58 percent versus 29 percent). An estimated 23 percent of dual enrollees use a mental health service at least once annually compared to 4 percent among other Medicare enrollees.16 The rate of hospital admissions per 1,000 people is 596 for dual enrollees versus 144 for other Medicare enrollees; the rate per 1,000 enrollees for emergency department visits is 780 for dual enrollees versus 434 for other Medicare enrollees.17

Given their extensive health care needs and utilization, the cost for dual enrollees is much greater compared to most non-dual enrollees. Dual enrollees account for 15 percent of the Medicaid population nationally but consume 33 percent of national Medicaid costs; they account for 20 percent of the national Medicare population but consume 34 percent of Medicare costs.18 A national study based on 2012 data found the average monthly combined Medicare and Medicaid cost for dual enrollees was $2,532; this was more than three times the cost to Medicare for Medicare-only beneficiaries ($747) and more than six times the cost to Medicaid for Medicaid-only beneficiaries ($401).19 A study based on 2013 data found average annual combined Medicare and Medicaid costs for dual enrollees were $29,258 with $18,112 from Medicare and $11,126 from Medicaid; this was about three times the cost for Medicare-only enrollees ($8,593) and seven times the cost for Medicaid-only enrollees ($4,021).20

The pattern of spending among dually enrolled can be described in terms of three subgroups. (1) Those with partial Medicaid benefits: This group has relatively low spending with a modest fraction of the total paid by Medicaid. (2) Those with full Medicaid benefits who do not require long-term care services: This group has somewhat higher total spending due to higher spending under Medicare and coverage of copayments and coinsurance and some supplementary services under Medicaid. (3) Those with full Medicaid benefits and requiring long-term care services: This group has high spending for acute care and for long-term care with expensive long-term care services covered by Medicaid.

Precise data are not available to flesh out the amount and distribution of costs for these three groups, but the range is suggested in 2009 national data indicating that combined Medicare and Medicaid spending for those with partial Medicaid benefits was less than half that for those with full benefits ($15,300 versus $34,800 annually for those over age 65), and among the partial benefits group the share paid by Medicaid was about 4 percent versus 45 percent among those with full benefits.21 For those with full benefits, the total cost and share paid by Medicaid is significantly higher among those requiring long-term care services. National data from 2013 indicate about 20 percent of those with full benefits use institutional long-term care and another 15 percent to 28 percent use some community based services; the per user added cost for these services is about $40,000 annually for institutional care, and $10,000 to $29,000 annually for the community based services, with all those added costs paid by Medicaid.22

The characteristics of the dually enrolled population in New York State likely follow the national patterns. In New York State dual enrollees comprise 15 percent of the Medicaid population but consume 36 percent of the program’s costs. Additional detailed data about the health status and utilization patterns of the State’s dually enrolled population are not available publicly.

Options for Coordinating Care for Dual Enrollees

Because of the significant health care needs and costs of the dual population, it has long been recognized that they could benefit greatly from enhanced coordination of care beyond that available in traditional fee-for-service medicine. Initiatives have been launched within the Medicaid program, within the Medicare program, and between the two programs to better manage care.

Options for Care Management within Medicaid

New York, like many states, has relied on managed care organizations (MCOs) to coordinate care for Medicaid enrollees. “Mainstream” MCOs enroll most Medicaid enrollees and assume responsibility for delivering and coordinating a comprehensive set of services in exchange for a fixed capitation payment from the State. New York’s managed care initiative began with limited enrollment in 1988 and was made mandatory for a wider population in the 1990s. In 2010 the MRT began initiatives to expand the scope of services covered by mainstream MCOs and to extend mandated enrollment to a broader population; in 2012 initiatives were launched to create specialized MCOs (known as Health and Recovery Plans or HARPs) to serve those with significant behavioral health issues. Between 2010 and 2018 the number of enrollees in mainstream MCOs increased from 3.1 million to 4.3 million and the share of spending for this population paid for through MCOs increased notably as prescription drugs, home care, and a variety of other services were moved into the MCO benefit package.23

However, dual enrollees generally did not participate in this movement to managed care. Two factors explain their exclusion. First, federal Medicare rules prohibit mandating managed care enrollment among Medicare enrollees. Any enrollment would have to be voluntary, and this typically is limited. Second, the State seeks to avoid paying for Medicare covered services under its Medicaid program, because Medicare is fully federally funded while Medicaid divides costs between the two governments. Since MCOs cover many Medicare covered services, enrolling dual enrollees in Medicaid Managed Care plans would benefit fiscally the federal government and cost the State.

It is worth noting the exclusion of dual enrollees from mainstream MCOs creates a disruption in continuity of care for mainstream MCO enrollees when they become age 65. Medicaid enrollees are automatically disenrolled from mainstream MCOs when they reach the age of 65. The newly dually eligible person then either obtains Medicare and Medicaid services under fee-for-service arrangements or voluntarily enrolls in a Medicare-sponsored managed care arrangement such as an Advantage plan; the individual cannot remain in a Medicaid MCO. Although Medicare serves as the primary payer for dual enrollees regardless of their Medicaid enrollment type, care management services provided by the State may result in greater fiscal benefits to the federal government than the State as Medicare-covered services are reduced and/or replaced by Medicaid-covered services.

New York has developed three options to better coordinate care for the dually enrolled under its Medicaid program that adjust to the two factors noted above – Managed Long-term Care (MLTC) plans, Health Homes, and Patient Centered Medical Homes (PCMH).

Managed Long-term Care Plans

MLTC plans cover only long-term care services funded by Medicaid; the plans receive a capitation payment from the State for these services and manage and coordinate long-term care services with acute services in a manner intended to be more effective than under fee-for-service arrangements. Prior to the MRT enrollment in MLTC plans was voluntary; from 2012 through 2015 mandatory MLTC was phased in for all dually enrolled individuals older than age 21 who require at least 120 days of long-term care services per year. Duals between the ages of 18 and 21 with similar long-term care needs may voluntarily enroll.24 Largely because of the MRT mandate from 2010 to 2018 enrollment in MLTC plans increased from 42,523 to 199,281.25

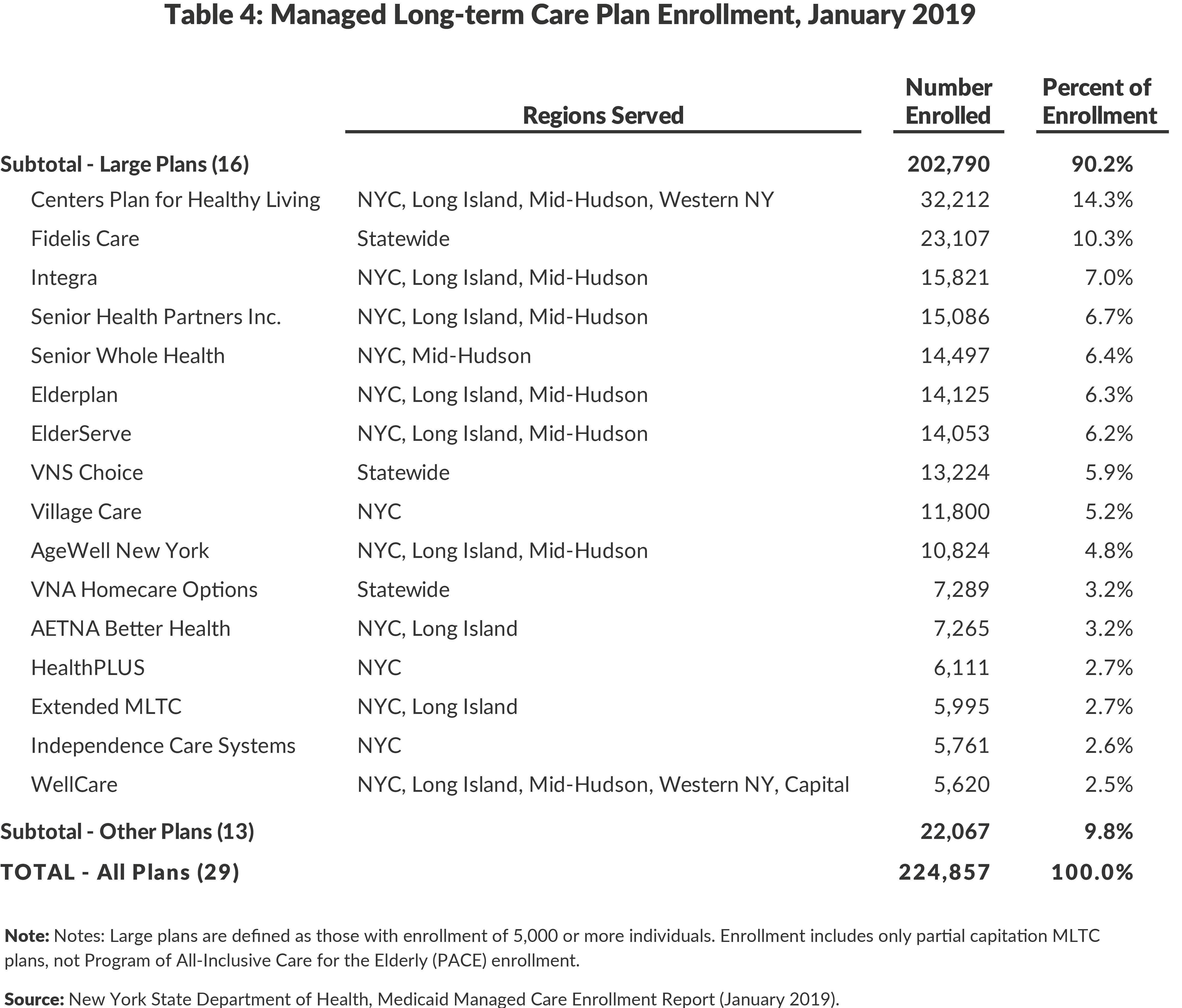

In January 2019, 29 MLTC plans were available in New York. At least one plan is available in each county in the State, and all counties have some enrollment. As shown in Table 4, the 16 plans with the largest enrollment, at least 5,000, account for nine of every ten enrollees.

New York’s MLTC initiative is one of more than 40 programs in 24 states using the strategy of managed care for long-term care services. Most are more recent than New York’s, and limited evaluation results are available. An evaluation of Texas’ program found a 3.5 percent decrease in cost compared to expected fee-for-service results, and a study of Minnesota’s program found reductions in hospitalizations and emergency room visits. A national evaluation of all programs has been commissioned, focusing on the New York and Tennessee programs because they have the best data for meaningful impact analysis. Results will be reported in 2019, but preliminary findings suggest positive impacts in New York.26

Health Homes

Health homes are a care coordination service for Medicaid enrollees with multiple chronic conditions, mental health or substance abuse diagnoses, and serious mental illness. A health home provides an enrolled beneficiary with a care manager who helps the enrollee receive needed care and services. The health home model leverages coordination among varying providers and can also link the beneficiary with non-clinical support services.

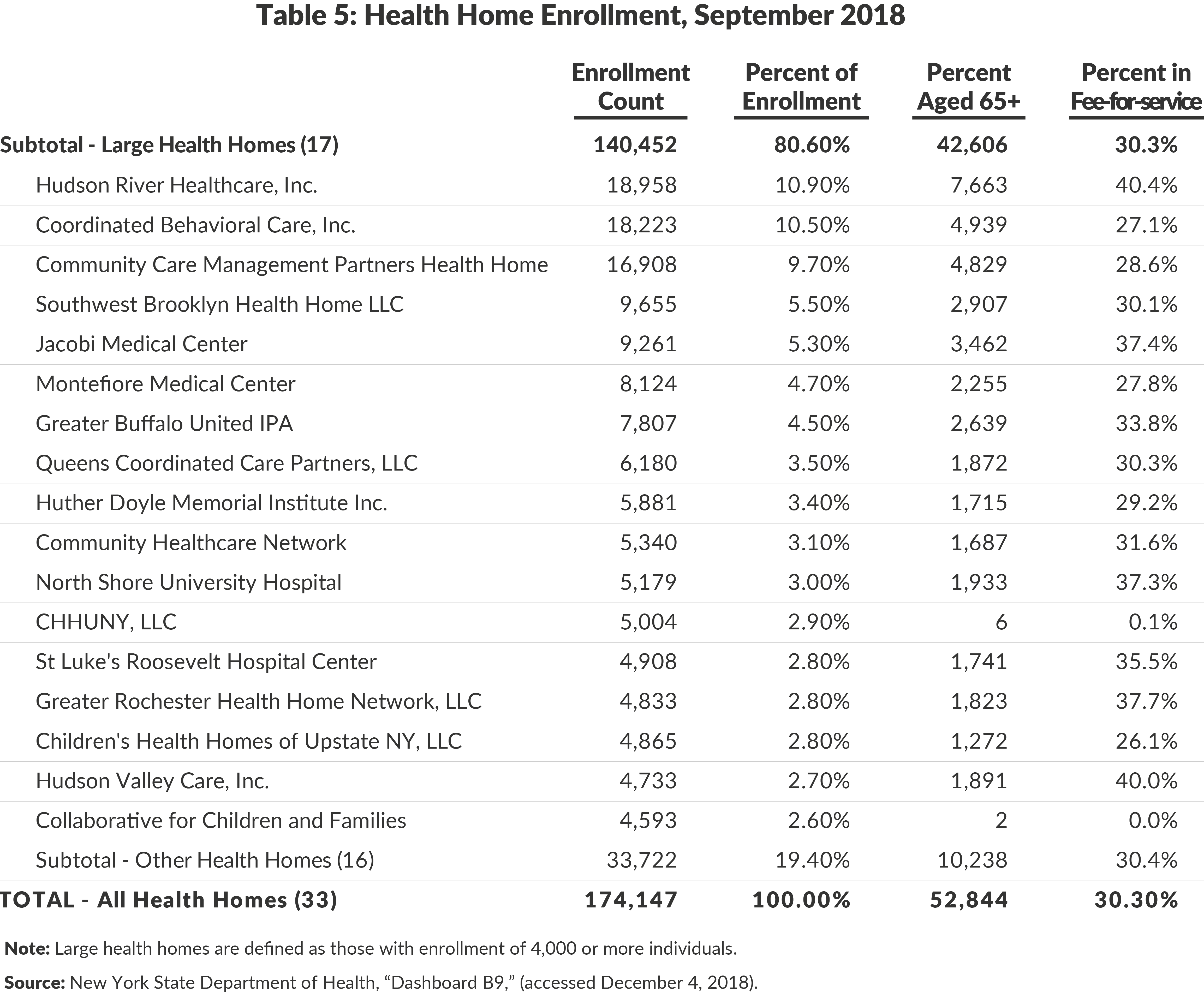

Health homes launched in New York in 2012 following passage of the federal Affordable Care Act (ACA), which set standards for health homes and offered states 90 percent federal funding for the first two years of health home services. The New York model built on existing care coordination programs for specific subpopulations.27 Initially approximately 1 million Medicaid enrollees were viewed as eligible for the health home program, and about one-third of those were dually enrolled individuals. However, after more than five years only approximately 170,000 people enrolled.28

In 2018 nearly 53,000 dually eligible persons were enrolled in a health home, about 30 percent of the total health home population. Among the dually eligible individuals in a health home 61 percent were younger than age 65 and presumably eligible due to disability.29

As shown in Table 5, 17 relatively large health homes each with more than 4,000 enrollees account for more than 80 percent of the total enrollees and 80 percent of the dually eligible enrollees with the other 20 percent divided among 16 smaller entities. For most plans between one-quarter and 40 percent of enrollees are dually eligible.

The low enrollment in health homes relative to the initial target has been attributed to multiple factors. Enrollment was voluntary, marketing and outreach efforts were poorly targeted, some payment rates were inappropriate, and coordination between Health Homes and MCOs (and their electronic record systems) had gaps. The New York State Department of Health (DOH) and health home organizations are working to improve and expand the program with growing potential for serving dual enrollees.30

Although health home programs have been established in 20 other states and the District of Columbia, little evaluation of impacts has been completed. DOH has commissioned an independent evaluation of its program, but no results have been reported publicly to date. Evaluations of other state programs indicate those programs are more targeted to specific populations than New York’s, notably to those with severe mental illness; that enrollment targets were reached more closely in other states by building on existing relationships between care management agencies; and favorable results in terms of reducing unnecessary or inappropriate utilization were most likely among those with severe mental illness and with an extended period of continuous enrollment.31

Patient-Centered Medical Homes

The PCMH model coordinates care through a physician-led team that provides primary care and manages other care needs. A PCMH designation is given to providers (often primary care physician practices, clinics, and community health centers) which meet standards developed by the State and the National Committee for Quality Assurance (NCQA). In exchange for this care coordination, a PCMH receives a small enhanced per visit payment through the Medicaid program. Grant funds for the establishment and development of PCMHs were also made available by the federal and State governments.

PCMHs were authorized in New York State in 2009, and standards for participation are regularly updated. PCMH designation has become widespread in New York. As of December 2017 New York State had nearly 2,000 practices designated, and New York comprised 13.6 percent of the nation’s PCMH practices.32 As the number of practices designated as PCMHs has risen, the penetration of the PCMH model has increased in terms of enrollees; 59 percent of Medicaid Managed Care enrollees are assigned to a PCMH provider.33 It is not reported publicly how many dually enrolled Medicaid enrollees use a PCMH.34

A PCMH is intended to reduce costs, improve health status, and improve the patients’ health care experience. Early evaluations of the model find some improvements on all three goals.35 Evaluations of specific pilot programs found reductions in emergency department use and costs.36

While the PCMH is a promising model for many Medicaid enrollees, its relevance for dual enrollees may be more limited. The model appears best suited to those with low acuity levels who rely mostly on primary care physicians for medical services. Those, like many dual enrollees, with multiple chronic conditions and behavioral health problems requiring care by multiple physicians and specialists may justify more intensive care coordination efforts such as those provided by health homes.

Options for Care Management within Medicare

The Medicare program has developed two basic strategies for improving care management for its enrollees. For those served through fee-for-service arrangements, it has promoted Accountable Care Organizations (ACOs). As an alternative to fee-for-service arrangements, it has supported capitated managed care plans, known as Medicare Advantage plans.

Accountable Care Organizations

ACOs are networks of providers who agree to deliver services to a defined population of Medicare beneficiaries. They are paid under Medicare fee-for-service arrangements, but annually may receive additional payments based on savings achieved relative to benchmark costs which are calculated based on the acuity of the beneficiary and historical costs.37 Savings are expected to be achieved through greater care coordination resulting in reduced use of hospital inpatient and emergency services; improved quality of care is expected through patient education, engagements, and outreach. Multiple versions of the program have been offered with the ACOs potential bonus varying with the degree of risk they accept for potential losses due to higher cost than the comparison group. Nationally the number of ACOs has grown from 220 in 2013 to 561 in January 2018 with 10.5 million Medicare beneficiaries in the program at the start of 2018.38 All participation in ACOs is voluntary with recruitment by the ACO.39

In New York the first Medicare ACO launched in 2012, and 36 were operating by 2017. Approximately 576,000 Medicare enrollees receive their health care through these ACOs. Of the 36 plans, 4 were new in 2017; among the 32 plans operating in 2016 enrollment varied from 6,051 to 74,386, and the six largest plans with more than 30,000 enrollees each accounted for 45 percent of the enrollment.40 The number of dual enrollees in ACOs is not reported publicly, but duals are not likely to account for a large share of the enrollment.

ACO performance in New York in terms of achieving savings has been disappointing. Only 5 of the 32 ACOs received bonus payments for 2016; the others either achieved insufficient savings to earn a bonus (7 plans), or incurred losses relative to the benchmark (20 plans). In the aggregate the ACOs provided costlier care compared to benchmarks; in 2016 the 32 ACOs exceeded benchmark costs by 1 percent.41

Medicare Advantage Plans

Medicare managed care options are known as Advantage plans, and for this analysis the Advantage plans may be divided into three types: (1) the “regular” plans that provide all Medicare benefits but make no special arrangement for the dually eligible; (2) Advantage Dual Special Needs Plans (D-SNPs) that supplement the Medicare benefits with coordination services to help access Medicaid benefits but rely on state Medicaid fee-for-service payments to providers to finance the Medicaid benefits; and (3) Medicaid Advantage plans that include Medicaid benefits in their packages as well as Medicare benefits and receive funding from state Medicaid agencies to cover the cost of the Medicaid services.

While some dual enrollees with partial benefits may enroll in regular plans, these plans are intended primarily to serve a Medicare-only population. In 2017 among the nearly 3.6 million Medicare beneficiaries statewide, about 1.4 million or 39 percent were in some form of Advantage plan with about 1.1 million in regular plans. These plans account for more than 80 percent of all Advantage plan enrollment statewide, with plans for the dually enrolled representing the other 20 percent.42

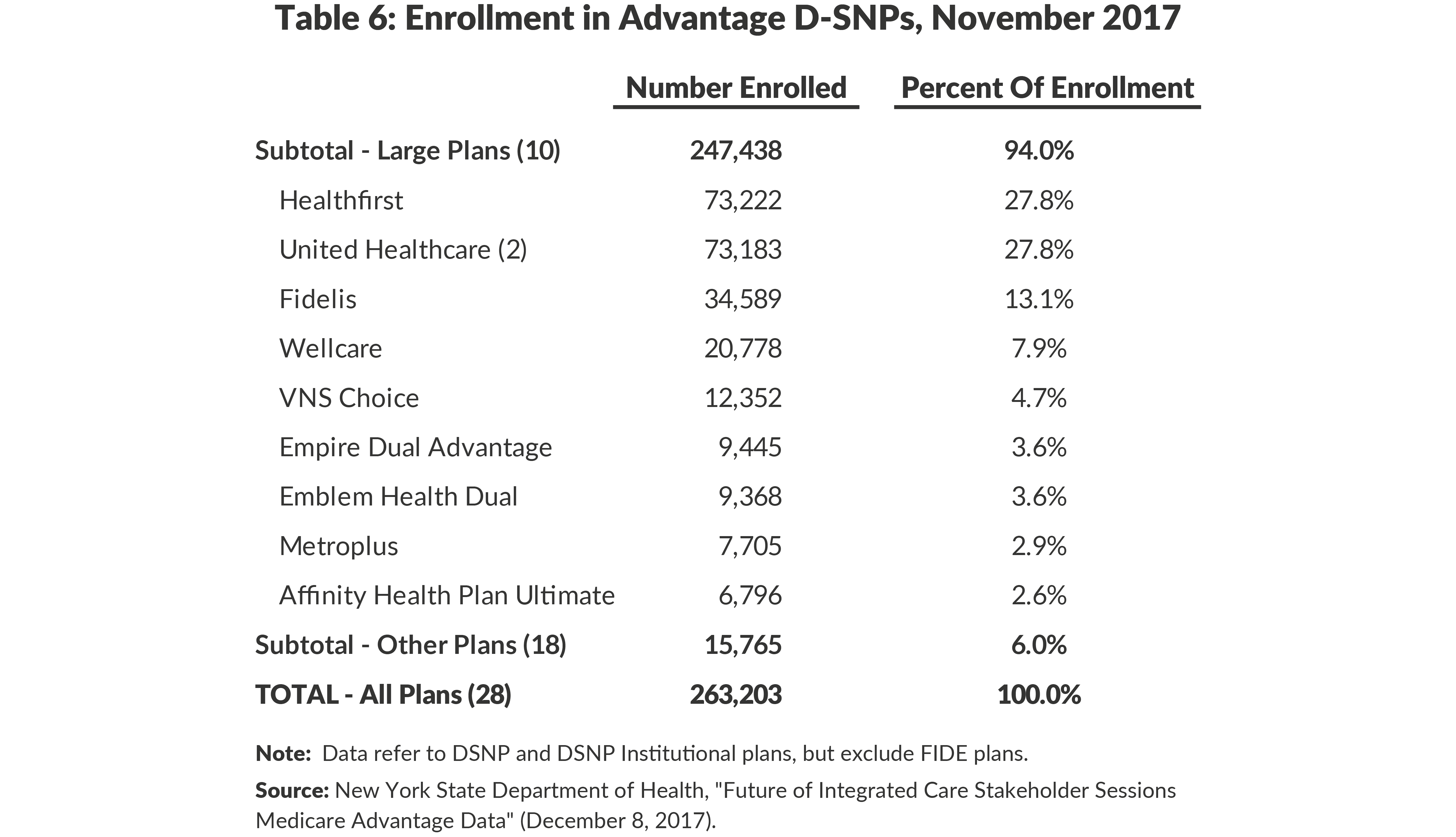

The Advantage D-SNPs have more than 260,000 enrollees. They are divided among 28 different plans. Enrollment varies notably with two plans having less than 100 enrollees and the largest plan with more than 70,000. As shown in Table 6, the 10 largest plans have 94 percent of the total enrollment.

Nationally in 2016, 356 Advantage D-SNPs existed in 38 states, Puerto Rico, and the District of Columbia.43 A 2008 evaluation of the initial D-SNPs (launched in 2006) found they were growing and attractive to the industry, but indicated it was too early to determine if they improved beneficiary health outcomes, and found no evidence that they were yielding savings for the Medicare program.44 In 2013 the Medicare Payment Advisory Commission (MedPAC) reviewed the D-SNP experience in advance of the Congressional deadline for renewal of the program. They recommended against renewing the program in its current form on grounds that it was not integrating care sufficiently to achieve quality improvements or cost savings. They found some effective models that integrated Medicaid and Medicare benefits and recommended renewal only for plans “that assume clinical and financial responsibility for Medicare and Medicaid benefits and allow authority for all other D-SNPs to expire.”45 The authorization was extended permanently largely in its current form which requires only that D-SNPs have some coordination with Medicaid but no mandatory coverage of Medicaid benefits.

Some states are promoting more effective use of D-SNPs by using Medicaid procurement practices in effect to mandate coordination between Medicaid MLTC plans and Advantage D-SNPs. At least 10 states require an MLTC to offer a companion D-SNP, and at least 6 states do not sign contracts with an Advantage D-SNP unless the company also has a Medicaid MLTC plan. Three states prohibit their D-SNPs from enrolling a person who is not enrolled in that company’s companion Medicaid plan.46

New York State has developed a version of a D-SNP that covers Medicare benefits and Medicaid long-term care services. The federal model, known as a Fully Integrated Dual Eligible Special Needs Plan (FIDE-D-SNP) is called Medicaid Advantage Plus in New York. Because it combines Medicare and Medicaid benefits in one plan, it is described in the next section.

Options for Care Management Combining Medicaid and Medicare

Four options have been developed under which a combination of Medicaid and Medicare benefits are offered by a single plan: Program of All-Inclusive Care for the Elderly (PACE) plans, Medicaid Advantage plans, Medicaid Advantage Plus (MAP) plans, and Fully Integrated Dual Advantage (FIDA) plans.

Program of All-Inclusive Care for the Elderly

PACE is the oldest form of an integrated plan. It was started as a demonstration project in the early 1980s and was permanently authorized in 1997. PACE plans use a distinctive model of care based on adult daycare centers staffed by an interdisciplinary team that provides a range of services including medical care. PACE plans cover all Medicare and Medicaid benefits, and the plans receive a capitation rate set under a three-way contract among the plan, Medicare, and the state Medicaid program. Enrollment is limited to persons age 55 or older who need the level of care provided in a nursing home, but the program seeks to avoid nursing home placement. Enrollment is voluntary and not tied to dual eligibility, but the vast majority of enrollees are dually enrolled.

Nationally 124 PACE plans operate in 31 states with a total enrollment of more than 41,000.47 In New York nine PACE plans have a total enrollment of 5,657. The largest plan has 2,849 enrollees, and the others range from 105 to 766.48 PACE plans tend to be operated by nonprofit organizations rather than commercial insurance plans.

Evaluations of PACE plans have found they provide high quality care and avoid nursing home placements, but they have costs higher than combined Medicaid and Medicare expenses for comparable populations. The higher costs are attributed to capitation rates set above the cost of comparable fee-for-service costs and above standard Advantage plan rates. The MedPAC has recommended facilitating expansion of PACE plans by conforming their rate-setting method to that of Advantage plans, opening enrollment to those younger than age 55, and creating an outlier protection program for enrollees with unusually high costs.49

Medicaid Advantage Plans

Medicaid Advantage plans are a combination of a Medicaid MCO with benefits similar to a mainstream MCO and a Medicare Advantage plan. They provide the combined set of benefits and receive separate capitation rates from the Medicaid and Medicare programs to cover relevant costs. To facilitate coordination the plans establish a coordination of benefits (COB) agreement, which clarifies their health care delivery and payment responsibilities. Generally they establish Medicare as the primary payer for services otherwise covered by Medicaid and Medicare.

New York has four Medicaid Advantage plans with a total enrollment of 6,520. Enrollment in the individual plans ranges from 354 to 2,998.50 Medicaid Advantage plans have voluntary enrollment with marketing by the plans; enrollment has remained low with few people opting for them.

Medicaid Advantage Plus Plans

MAP plans combine services covered by Medicare with comprehensive Medicaid services including long-term care. The MAP option in effect combines a Medicare Advantage plan and a Medicaid MLTC plan in a single package. The plans receive capitation rates from the Medicaid and Medicare programs to cover the cost of relevant benefits. Enrollment is voluntary with marketing by the plans and targeted to those dual enrollees with long-term care needs; a MAP plan can substitute for a Medicaid MLTC plan under the State’s requirement for mandatory MLTC coverage. The MAP level of integration requires a single three-party contract, and it aligns the plans more significantly than the COB agreement of Medicaid Advantage plans.

Enrollment in MAP plans has been increasing; between March 2018 and March 2019 enrollment increased 50 percent, from 9,812 to 14,838. Currently seven are active, but three plans have enrollment of less than 100. One large plan (Healthfirst) accounts for nearly two-thirds of total enrollment.51 Growing the plans has been difficult. Most of those eligible are already enrolled in Medicaid MLTC plans and use traditional Medicare fee-for service arrangements for Medicare services; switching to a MAP plan in effect requires exchanging Medicaid and Medicare cards for the plan enrollment and network limits. In addition enrollment is complicated by different processes and timetables for Medicare and Medicaid benefits within the single plan.

Fully Integrated Duals Advantage Plans (FIDA)

FIDA plans are a relatively new model created under a federal demonstration program that began implementation in 2013. FIDA plans combine all Medicaid and Medicare benefits using one three-way contract among the plan, the State, and the federal Medicare program. Requirements for care coordination are more extensive than under D-SNPs, calling for an interdisciplinary team to do an initial assessment and care plan and monitor services. Under the FIDA demonstration states were allowed to use passive enrollment, assigning Medicaid beneficiaries to a plan but allowing them to opt out, rather than requiring plans to market individually as under Medicare Advantage rules. FIDA plans also were designed to have integrated enrollment and appeals processes rather than separate processes for each program.

Between 2013 and 2015 demonstrations were launched in 13 states with initial plans to last three years. Two states discontinued their programs after three years, and most of the other states have extended their programs to periods of four or five years with ending dates in 2019 or 2020.52

The demonstrations have faced three common challenges, each of which has been severe in New York. First, despite the availability of passive enrollment, participation has been low. Overall 29 percent of eligible beneficiaries enrolled, with rates varying from 68 percent in Ohio to just 3 percent in New York. Ohio was the only project to have a participation rate greater than 50 percent. The low participation likely is due to individuals’ satisfaction with their current care, their lack of understanding of the nature of the FIDA plans and their potential benefits, and in some cases current providers encouraging them to opt out.53

Second, some plans have withdrawn from the program. Initially 68 plans participated nationwide, but 18 plans have left, of which 11 were in New York. The primary reason for withdrawal is low enrollment; all 11 plans leaving the New York demonstration had fewer than 300 enrollees while estimates are that 5,000 to 7,500 enrollees are needed to make a plan viable. Some early withdrawals were attributed to low capitation rates, but the Medicare program adjusted its rate-setting methods in 2016, and this is no longer considered an issue.54

Third, the care coordination requirements were considered too burdensome by some plans. The initial standards required the interdisciplinary teams to meet in person and to include the primary care physician; some physicians found this too time consuming. The requirements were modified in New York, but many plans still consider the administrative requirements burdensome.

The federal Medicare agency has commissioned an independent evaluation of the demonstrations, with a mandate to identify impacts on access to care, service use, quality of care, and cost. Results of the evaluation are not yet available and are not expected for another two or more years due to the extension of the demonstration period and difficulties in assembling the required data for quantitative analysis. Interim evaluation reports have described the care coordination process and patient experiences with plans.55

In its 2018 Report to Congress the MedPAC reached this interim conclusion about the FIDA approach: “…much of the information that is currently available, while limited, is relatively positive. Enrollment is stable, quality of care appears to be improving, payment rates appear adequate, plans have grown more confident about their ability to manage service use, and stakeholders remain supportive of the demonstration.”56

However, New York may be an exception to this general observation. Its participation rate is extremely low, and enrollment remains at a level that may not be sustainable for some plans. As of March 2019 the seven remaining active plans had a combined enrollment of less than 3,000. Two plans–Healthfirst and VNSNY–had enrollment of more than 1,000 each, totaling 2,313 of the 2,941 statewide enrollees (79 percent). The other five plans reported enrollment ranging from 1 to 442.57

These problems persist despite efforts to revise the program. FIDA enrollment has decreased each month since October 2015. New York State offered some fixes in December 2015.58 Then in September 2016 the State held outreach webinars for potential providers and beneficiaries.59 At the same time, the State published informational brochures for plans and providers to attempt to help with outreach.60 In November 2016 the State announced the FIDA demonstration had been extended two years to the end of 2019, signaling the State’s intent to continue the program at least in the short-term.61 After the State announced the extension, a series of stakeholder engagement meetings were convened to consider the future of FIDA and other programs for duals. The Future of Integrated Care series brought participants together to review existing options and to consider opportunities for the models. The sessions were convened by DOH throughout 2017. Among the topics covered were reimbursement issues, enrollment barriers, provider concerns, and geographic scope.62 The series has yet to yield a promulgated set of recommendations on how to move forward.

Options for Future Strategies

Improving care for the dually eligible population remains a serious and important challenge. The population is growing, has extensive medical care needs, incurs high costs of care, and often receives poorly coordinated care. Numerous approaches have been tried, but the evidence supporting the alternative models is mixed and limited. In confronting the hard choices, five options–not necessarily mutually exclusive–can be identified.

Strategy #1: Revitalize the FIDA model

In many respects the FIDA demonstration incorporates an optimal model of care integration. It establishes a single plan to provide Medicare and Medicaid benefits, sets high standards for care coordination, integrates enrollment and appeals processes, and provides financial incentives for efficient care. Yet most observers consider the demonstration unsuccessful due to the low enrollment and plan participation, and revitalization likely is not a viable option.

However it is instructive to extract some lessons from the FIDA demonstration experience. A core problem is the low enrollment; passive enrollment did not work as effectively as expected. Two types of changes appear necessary. First, the plans should be better marketed with more extensive consumer education. Prior to any passive enrollment, beneficiaries and their families should receive information about any new integrated plans and their potential benefits.

Second, the competition from alternative care arrangements should be constrained. Most of those opting out have remained with current MLTC plans. (See Table 7.) The competitive options could be constrained by not allowing integrated plan sponsors to offer MLTC plans. Of the 10 FIDA plans, 8 are sponsored by entities that also offer MLTC plans; their combined MLTC enrollment exceeds 67,000 and moving enrollees to FIDA plans would have increased dramatically FIDA enrollment. More drastically, competition from MLTC plans could be eliminated by requiring them to convert to integrated arrangements. Such measures are difficult and will face opposition from current providers.

Strategy #2: Build on the Medicaid Advantage and Medicaid Advantage Plus Models

The Medicaid Advantage and MAP models provide a high degree of integration of care, and together they serve both those with significant long-term care needs and others with multiple conditions but not requiring significant long-term care. However, the plans have experienced limited enrollment due to the lack of integration in enrollment process described previously and to competition from alternative arrangements.

Building on these models can draw on the lessons from the FIDA demonstration. Enrollment and appeals processes can be better integrated, and passive enrollment can be improved with marketing material and pairing enrollees currently in MLTC plans with MAP plans offered by the same corporate sponsor.

Limits on competition from alternative plans may also be appropriate (See Table 7.) For those requiring long-term care, MAP enrollment in eight available plans totals about 11,000, compared to more than 200,000 in 29 MLTC plans and another 20,000 in other options such as PACE plans and D-SNPs for those in nursing homes. Constraints on competition from MLTC plans could include requiring entities sponsoring Medicaid Advantage Plus plans to not offer MLTC plans; seven of the eight MAP plans are sponsored by entities with MLTC plans, and their combined MAP and MLTC enrollment is about 82,000. A more drastic approach would be to require all MLTC plans to be converted to MAP plans.

For those not requiring long-term care, Medicaid Advantage enrollment in four available plans is less than 7,000 compared to D-SNP enrollment of about 245,000 in 19 plans and an even larger group in fee-for-service arrangements that includes more than 50,000 served by 33 health homes. Marketing material from DOH explaining the benefits of each option for individuals with various types of health conditions could be helpful for the dually eligible population in making their enrollment decisions. Competition from D-SNPs could be limited by requiring entities sponsoring Medicaid Advantage plans to not offer D-SNPs; all four of the Medicaid Advantage plan sponsors offer D-SNPs with a combined enrollment of nearly 130,000.

Expanding the Medicaid Advantage and MAP models faces serious challenges due to the current competition. Limiting the competition likely would face opposition from those plan sponsors. In addition individuals with narrowed choices might opt for fee-for-service arrangements rather than move from D-SNPs to Medicaid Advantage plans.

Strategy #3: Expand partnerships between Medicare Advantage D-SNPs and Medicaid MLTC plans

The two largest sources of coordinated care are MLTC plans and Advantage D-SNPs; in New York 29 MLTC plans serve more than 200,000 individuals, and D-SNPs serve more than 250,000 dual enrollees. The services of the two types of plans are not duplicative and can be complementary; MLTC plans deal with long-term care services under Medicaid, and D-SNPs deal with acute care services available under Medicare and Medicaid. The extent to which MLTC enrollees also participate in D-SNPs is not reported publicly, but more can be done to coordinate the plans’ respective services by encouraging partnerships between the two types of plans.

This strategy differs from the previous strategy in two important ways. First, it relates only to those with significant long-term care needs; dual eligible with other conditions requiring better care coordination would not be reached. Second, individuals would be served by two different plans rather than a single integrated plan. This may be preferable to current arrangements involving an MLTC plan combined with Medicare fee-for-service, but would offer less integration than a single MAP plan.

Other states use a variety of practices to encourage such partnerships, sometimes called “aligned enrollment.”63 Options include:

- Require MLTC plans to offer companion D-SNPs in their service area. In New York in 2018 only 9 of the 29 entities sponsoring MLTC plans also sponsored a D-SNP.

- Limit contracting with D-SNPs to plans also having MLTC plans. In New York in 2018 nine of the D-SNP plans were sponsored by entities that did not also have an MLTC plan.

- Allow passive enrollment of MLTC plan members in aligned D-SNPs.

Establishing a pattern of aligned enrollment for those requiring long-term care services can be a substitute for fully integrated plans, allowing the Medicaid and Medicare programs to have separate contracts with the respective plans. Following this strategy should be accompanied by enhanced requirements for coordination between providers in the two plans. While D-SNPs already have some Medicaid coordination requirements, and these were expanded in 2018 federal legislation effective in 2021, the degree of integration could be further strengthened by State rules such as requiring common electronic medical records and shared care management plans. This approach may also help promote continuity of enrollment in both Medicaid and Medicare managed care plans, for which continuity of enrollment is a significant issue.64

Strategy #4: Target enrollment in health homes among eligible fee-for-service duals

Those dual enrollees without long-term care needs (and not enrollees with Intellectual or Developmental Disabilities, IDDs) typically receive their Medicaid and Medicare services in fee-for-service arrangements. Some may be in Advantage plans, but it is likely that between 300,000 and 400,000 dual enrollees are obtaining care in a fee-for-service market. Many in this group have Medicaid expenses limited to Medicare premiums and cost sharing, but some may have high Medicaid expenses for services not covered by Medicare. These individuals may have serious mental illness or other chronic conditions that require services beyond Medicare benefits.

Many of these dual enrollees could benefit from health home services. As shown earlier in Table 5 about 53,000 dually eligible individuals are already enrolled in health homes, and they comprise about 30 percent of the total health home enrollment. However, health home enrollment is below initial targets and many dual enrollees who might be priority candidates likely have not been reached. Targeted outreach and marketing to these beneficiaries tied to passive enrollment may yield significant health care improvements and cost savings. Health homes can also link their clients with non-clinical services and supports with benefits for enrollees such as those with serious mental illness.

While potentially appropriate for numerous dually eligible individuals, health homes provide more limited financial incentives for cost-effective care integration than does enrollment in risk-bearing managed care entitites such as D-SNPs and Medicaid Advantage plans. The strategy of expanding health home enrollment among the dually eligible should focus on those for whom it is most cost-effective.

Strategy #5: Support broader marketing of Medicare Advantage D-SNPs

While health homes may be appropriate for those with complex care needs, the large dually eligible population in the fee-for-service market likely includes many individuals who have less intensive needs but still can benefit from coordinated care. For this group better marketing of Advantage D-SNPs could engage them in these plans and improve their care at reasonable cost. Currently marketing of these plans is a responsibility of the plans; the State could supplement their efforts with educational campaigns and preparation of materials that could be shared by multiple plans.

One specific way to better market D-SNPs is to encourage enrollment among the current Medicaid MCO enrollees who reach age 65 and are discontinued from MCO enrollment. These individuals could be enrolled passively in D-SNPs sponsored by their MCO plan or partnered with that plan. About 58,000 MCO enrollees reach age 65 each year, and passive enrollment of this group in affiliated D-SNPs could expand D-SNP enrollment and provide better coordinated care to the individuals.65

Appendix

Footnotes

- Charles Brecher and Mina Addo, What Ails Medicaid in New York? (Citizens Budget Commission, May 2016), https://cbcny.org/research/what-ails-medicaid-new-york-0.

- Patrick Orecki, Challenges of Enhancing Effective Engagement of Community Based Organizations in Performing Provider Systems (Citizens Budget Commission, November 2017), https://cbcny.org/research/challenges-enhancing-effective-engagement-community-based-organizations-performing.

- Patrick Orecki, Options for Enhancing New York’s Health Home Initiative (Citizens Budget Commission, May 2018), https://cbcny.org/research/options-enhancing-new-yorks-health-home-initiative.

- New York State Office for People with Developmental Disabilities, “NYS DOH and OPWDD announce a partnership to improve care for individuals with intellectual and developmental disabilities (IDD) who are eligible for both Medicare and Medicaid (‘Medicare-Medicaid Enrollees’)” (press release, June 8, 2015), https://opwdd.ny.gov/news_and_publications/fida-idd-announcement.

- For more information on the plan to transition the I/DD population into managed care see: New York State Department of Health, Draft Transition Plan for Home and Community-Based Services (HCBS), Health Home Care Management for Individuals with Intellectual and/or Developmental Disabilities (I/DD), and the Development of Specialized Managed Care (February 21, 2018), www.health.ny.gov/health_care/medicaid/program/medicaid_health_homes/idd/1115/final_revised_draft_tranisiton_plan_feb_2018_for_publication.pdf.

- New York State Department of Health, “Current FIDA Trends and Future Enrollment Opportunities” (January 2016), www.health.ny.gov/health_care/medicaid/redesign/fida/2016-1-29_fida_trends.htm.

- New York State Department of Health, "Medicaid Program Enrollment by Month: Beginning 2009" (January 29, 2019), https://health.data.ny.gov/Health/Medicaid-Program-Enrollment-by-Month-Beginning-200/m4hz-kz.

- New York State Department of Health, Providing Integrated Care for New York’s Dual Eligible Members Stakeholder Discussion (December 17, 2018), p. 5. Link?

- Persons qualifying by age must also have been legal U.S. resident for five years; those without a history of Social Security contribution may be required to pay premiums for Part A. Persons qualifying by disability must have been receiving Social Security disability benefits for two years.

- Data are for 2009 and from Congressional Budget Office, Dual-Eligible Beneficiaries of Medicare and Medicaid: Characteristics, Health Care Spending and Evolving Policies (June 2013) Table 1, p. 5, www.cbo.gov/sites/default/files/113th-congress-2013-2014/reports/44308dualeligibles2.pdf.

- Centers for Medicare and Medicaid Services, “Medicare Enrollment Dashboard” (November 2018), www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/Dashboard/Medicare-Enrollment/Enrollment%20Dashboard.html.

- Medicare.gov, “Monthly premium for drug plans” (accessed November 21, 2016), www.medicare.gov/drug-coverage-part-d/costs-for-medicare-drug-coverage/monthly-premium-for-drug-plans.

- The asset test for eligibility is only required for those who are aged, blind, or disabled. New York State Department of Health, “Medicaid in New York State” (March 2019), www.health.ny.gov/health_care/medicaid/.

- New York State Department of Health, “Medicaid Excess Income ("Spenddown" or "Surplus Income") Program” (November 2010), www.health.ny.gov/health_care/medicaid/excess_income.htm.

- The MSPs set asset limits of $7,390 for a single person and $11,090 for a couple, but allow states to set more generous asset limits. New York sets no limit on assets. See: Medicare Payment Advisory Commission and Medicaid and CHIP Payment and Access Commission, Data Book: Beneficiaries dually eligible for Medicare and Medicaid (January 2018) Table 2, p. 6, www.macpac.gov/wp-content/uploads/2017/01/Jan18_MedPAC_MACPAC_DualsDataBook.pdf.

- MaryBeth Musumeci, Medicaid's Role for Medicare Beneficiaries (Kaiser Family Foundation, February 2017), www.kff.org/medicaid/issue-brief/medicaids-role-for-medicare-beneficiaries/.

- Centers for Medicare & Medicaid Services, "Medicare-Medicaid Linked Enrollee Analytic Data Source (MMLEADS) Public Use File" (September 19, 2017), www.cms.gov/Medicare-Medicaid-Coordination/Medicare-and-Medicaid-Coordination/Medicare-Medicaid-Coordination-Office/DataStatisticalResources/DataToolsResearchers.html.

- Centers for Medicare & Medicaid Services, Medicare-Medicaid Coordination Office Fact Sheet – February 2018 (February 2018), p. 1, www.cms.gov/Medicare-Medicaid-Coordination/Medicare-and-Medicaid-Coordination/Medicare-Medicaid-Coordination-Office/Downloads/MMCO_Factsheet.pdf.

- Centers for Medicare & Medicaid Services, "National Profile of Medicare-Medicaid dual Beneficiaries" (December 14, 2017), https://healthdata.gov/dataset/national-profile-medicare-medicaid-dual-beneficiaries.

- Medicare Payment Advisory Commission and Medicaid and CHIP Payment and Access Commission, Data Book: Beneficiaries dually eligible for Medicare and Medicaid (January 2018), Exhibit 21, p. 64, www.macpac.gov/wp-content/uploads/2017/01/Jan18_MedPAC_MACPAC_DualsDataBook.pdf.

- Congressional Budget Office, Dual-Eligible Beneficiaries of Medicare and Medicaid: Characteristics, Health Care Spending and Evolving Policies, (June 2013) Table 2, p. 7, www.cbo.gov/sites/default/files/113th-congress-2013-2014/reports/44308dualeligibles2.pdf.

- Medicare Payment Advisory Commission and Medicaid and CHIP Payment and Access Commission, Data Book: Beneficiaries dually eligible for Medicare and Medicaid (January 2018), Exhibit 24, p. 70, www.macpac.gov/publication/data-book-beneficiaries-dually-eligible-for-medicare-and-medicaid-3/.

- Enrollment based on average monthly enrollment in a mainstream managed care plan for 2010 and 2018 based on data from New York State Department of Health, "Medicaid Program Enrollment by Month: Beginning 2009" (August 24, 2018), https://health.data.ny.gov/Health/Medicaid-Program-Enrollment-by-Month-Beginning-200/m4hz-kzn3.

- New York State Department of Health, “Managed Long Term Care” (October 2018), www.health.ny.gov/health_care/managed_care/mltc/.

- Enrollment based on average monthly enrollment in a partial capitation managed long-term care plan for 2010 and 2018 based on data from New York State Department of Health, "Medicaid Program Enrollment by Month: Beginning 2009" (August 24, 2018), https://health.data.ny.gov/Health/Medicaid-Program-Enrollment-by-Month-Beginning-200/m4hz-kzn3.

- See: Medicaid and CHIP Payment and Access Commission, Report to Congress on Medicaid and CHIP (2018), Chapter 3: Managed Long-term Services and Supports: Status and State Adoption and Areas of Program Evolution, pp. 62-63, www.macpac.gov/wp-content/uploads/2018/06/Managed-Long-Term-Services-and-Supports-Status-of-State-Adoption-and-Areas-of-Program-Evolution.pdf.

- Elizabeth M. Pacthias, Andrew Detty, and Michael Birnbaum, Implementing Medicaid Health Homes in New York: Early Experience (United Hospital Fund, February 2013), p. 3, https://uhfnyc.org/assets/1351.

- New York State Department of Health, “Dashboard B9,” (accessed February 10, 2018), https://dsripdashboards.health.ny.gov/.

- Unpublished data provided by the New York State Department of Health for September 2018 indicate total health home enrollment of 174,147 with 52,844 Medicare enrolled. Of the Medicare group, 32,112 were under age 65 and presumably eligible due to disability.

- See: Patrick Orecki, Options for Enhancing New York’s Health Home Initiative (Citizens Budget Commission, May 2018), https://cbcny.org/research/options-enhancing-new-yorks-health-home-initiative.

- Brenda Spillman and others, Evaluation of the Medicaid Health Home Option for Beneficiaries with Chronic Conditions: Progress and Lessons from the First States Implementing Health Home Programs, Annual Report- Year Four (Urban Institute, April 2016), https://aspe.hhs.gov/basic-report/evaluation-medicaid-health-home-option-beneficiaries-chronic-conditions-progress-and-lessons-first-states- implementing-health-home-programs-annual-report-year-four.

- New York State Department of Health, New York State Patient Centered Medical Homes Quarterly Report (December 2017), p. 8, www.health.ny.gov/technology/innovation_plan_initiative/pcmh/docs/pcmh_quarterly_report_dec_2017.pdf.

- New York State Department of Health, New York State Patient Centered Medical Homes Quarterly Report (December 2017), p. 15, www.health.ny.gov/technology/innovation_plan_initiative/pcmh/docs/pcmh_quarterly_report_dec_2017.pdf.

- New York State Department of Health, “New York State Patient-Centered Medical Home (NYS PCMH)” (August 2018), www.health.ny.gov/technology/innovation_plan_initiative/pcmh/.

- U.S. Department of Health and Human Services, Early Evidence on the Patient-Centered Medical Home (February 2012), https://pcmh.ahrq.gov/sites/default/files/attachments/early-evidence-on-pcmh-white-paper.pdf.

- MB Rosenthal and others, “A Difference-in-Difference Analysis of Changes in Quality, Utilization and Cost Following the Colorado Multi-Payer Patient-Centered Medical Home Pilot,” Journal of General Internal Medicine, vol. 31, no. 3 (March 2016), pp. 289-296, www.ncbi.nlm.nih.gov/pubmed/26450279.

- For summaries of ACO benchmarking methodologies, see: National Association of ACOs, Financial Benchmarking (accessed March 29, 2019), www.naacos.com/financial-benchmarking.

- Centers for Medicare and Medicaid Services, “Medicare Shared Savings Program Fact Sheet” (January 2018), www.cms.gov/Medicare/Medicare-Fee-for-Sevice-Payment/sharedsavingsprogram/ about.html

- Medicare.gov, Accountable Care Organization & You (July 2016), www.medicare.gov/Pubs/pdf/11588-Accountable-Care-Organizations-FAQs.pdf.

- United Hospital Fund, Health Watch, “New York Medicare ACO Performance: Cost and Quality Results Raise Bigger Questions” (December 2017), https://uhfnyc.org/publications/881264.

- Centers for Medicare and Medicaid Services, “Medicare Shared Savings Program Fact Sheet” (January 2018), www.cms.gov/Medicare/Medicare-Fee-for-Sevice-Payment/sharedsavingsprogram/ about.html; Gregory Burke and Suzanne Brundage, Accountable Care in New York State: Emerging Themes and Issues, Special Report (United Hospital Fund, April 2015), https://nyshealthfoundation.org/resource/accountable-care-in-new-york-state-emerging-themes-and-issues/ and New York’s Medicare ACOs: Participants and Performance, Data Brief (United Hospital Fund, April 2015), https://nyshealthfoundation.org/wp-content/uploads/2017/11/new-york-medicare- acos-participants-and-performance.pdf; and United Hospital Fund, Health Watch, “New York Medicare ACO Performance: Cost and Quality Results Raise Bigger Questions” (December 2017), https://uhfnyc.org/publications/881264.

- New York State Department of Health, “Future of Integrated Care Stakeholder Sessions Medicare Advantage Data” (December 8, 2017), www.health.ny.gov/health_care/medicaid/redesign/future/docs/2017-12-8_foic.pdf.

- Integrated Care Resource Center, State Contracting with Medicare Dual Eligible Special Needs Plans: Issues and Options, Technical Assistance Tool (November 2016), Exhibit 2, p. 4, www.chcs.org/media/ICRC_DSNP_Issues_Options.pdf.

- Robert Schmitz and others, Evaluation of Medicare Advantage Special Needs Plans, Summary Report (Mathematica Policy Research, Inc., September 30, 2008), www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/Reports/downloads/Schmitz2008.pdf.

- Medicare Payment Advisory Commission, Report to the Congress: Medicare Payment Policy (March 2013), p. 326, http://medpac.gov/docs/default-source/reports/mar13_entirereport.pdf.

- See Integrated Care Resource Center, “Tips to Improve Medicare-Medicaid Integration Using D-SNPs: Promoting Aligned Enrollment,” (April 2018) www.integratedcareresourcecenter.com/sites/default/files/ICRC_DSNP_Aligning_Enrollment.pdf; and Medicare Payment Advisory Commission, Report to Congress: Medicare and the Health Care Delivery System, June 2018, Chapter 9, “Managed Care Plans for Dual-Eligible Beneficiaries,” pp 268-269, http://medpac.gov/docs/default-source/reports/jun18_medpacreporttocongress_sec.pdf?sfvrsn=0.

- Medicare Payment Advisory Commission, Report to the Congress: Medicare and the Health Care Delivery System (June 2018), pp. 266-267, http://medpac.gov/docs/default-source/reports/jun18_medpacreporttocongress_sec.pdf?sfvrsn=0.

- New York State Department of Health, “Managed Long-term Care Enrollment by Plan, County and Program,” June 2018, www.health.ny.gov/health_care/managed_care/reports/enrollment/monthly/2018/docs/en06_18.pdf.

- Medicare Payment Advisory Commission, Report to the Congress: Medicare and the Health Care Delivery System (June 2012), www.medpac.gov/docs/default-source/reports/jun12_entirereport.pdf, and Report to the Congress: Medicare and the Health Care Delivery System (June 2018), pp. 266-267, http://medpac.gov/docs/default-source/reports/jun18_medpacreporttocongress_sec.pdf.

- New York State Department of Health, "Medicaid Program Enrollment by Month: Beginning 2009" (January 29, 2019), https://health.data.ny.gov/Health/Medicaid-Program-Enrollment-by-Month-Beginning-200/m4hz-kzn3.

- New York State Department of Health, “Medicaid Managed Care Enrollment Reports” (March 2019), www.health.ny.gov/health_care/managed_care/reports/enrollment/monthly/.

- Medicare Payment Advisory Commission, Report to the Congress: Medicare and the Health Care Delivery System (June 2018), p. 247, http://medpac.gov/docs/default-source/reports/jun18_medpacreporttocongress_sec.pdf?sfvrsn=0.

- Medicare Payment Advisory Commission, Report to the Congress: Medicare and the Health Care Delivery System, June 2018, p. 251, http://medpac.gov/docs/default-source/reports/jun18_medpacreporttocongress_sec.pdf?sfvrsn=0.

- Medicare Payment Advisory Commission, Report to the Congress: Medicare and the Health Care Delivery System (June 2018), pp. 254-255, http://medpac.gov/docs/default-source/reports/jun18_medpacreporttocongress_sec.pdf?sfvrsn=0.

- Medicare Payment Advisory Commission, Report to the Congress: Medicare and the Health Care Delivery System, (June 2018), p. 256, http://medpac.gov/docs/default-source/reports/jun18_medpacreporttocongress_sec.pdf?sfvrsn=0.

- Medicare Payment Advisory Commission, Report to the Congress: Medicare and the Health Care Delivery System (June 2018), p. 264, http://medpac.gov/docs/default-source/reports/jun18_medpacreporttocongress_sec.pdf?sfvrsn=0.

- New York State Department of Health, “Managed Long-term Care Enrollment by Plan, County and Program” (March 2019),www.health.ny.gov/health_care/managed_care/reports/enrollment/monthly/2019/docs/en03_19.pdf.

- New York State Department of Health, “FIDA Reform Letter” (December 9, 2015), www.health.ny.gov/health_care/medicaid/redesign/fida/2015-12-09_fida_reform_letter.htm.

- New York State Department of Health, “Fully Integrated Duals Advantage (FIDA)” (September 2016), www.health.ny.gov/health_care/medicaid/redesign/fida/outreach/ad_update_webinar.htm.

- New York State Department of Health, “FIDA Brochure” (September 2016), www.health.ny.gov/health_care/medicaid/redesign/fida/outreach/brochure.htm.

- New York State Department of Health, “FIDA Demonstration Extension Announcement” (November 9, 2016), www.health.ny.gov/health_care/medicaid/redesign/fida/mrt101/2016-11-09_demo_ext.htm.

- New York State Department of Health, “Planning for the Future of Integrated Care in New York State” (January 2018), www.health.ny.gov/health_care/medicaid/redesign/future/index.htm.

- See: Integrated Care Resource Center, “Tips to Improve Medicare-Medicaid Integration Using D-SNPs: Promoting Aligned Enrollment” (April 2018), www.integratedcareresourcecenter.com/sites/default/files/ICRC_DSNP_Aligning_Enrollment.pdf.

- See: David J. Meyers and others, Analysis of Drivers of Disenrollment and Plan Switching Among Medicare Advantage Beneficiaries (JAMA Internal Medicine, February 25, 2019), https://jamanetwork.com/journals/jamainternalmedicine/article-abstract/2725083.

- New York State Department of Health, “Providing Integrated Care for New York’s Dual Eligible Members” (presentation to invited attendees, December 17, 2018).