To Weather a Storm

Create an NYC Rainy Day Fund

Economic downturns and unforeseen emergencies can disrupt municipal budgets by reducing expected revenues and imposing unplanned costs. The most prudent approach to avoid the harmful consequences of such events is to have a rainy day fund (RDF) with resources to cover a significant portion of the adverse developments. However, New York State law enacted in the wake of the City’s fiscal crisis in the 1970s and provisions more recently incorporated into the City Charter require a balanced budget, which prevents New York City from using an RDF. The practices adopted by City officials to build reserves within the confines of legal restrictions are deficient. A better approach is to amend State law and the City Charter to permit use of an RDF, which should have:

- Sufficient resources to ameliorate the most damaging impacts of tax revenue losses due to a recession;

- Requirements for regular deposits to build and to sustain an RDF balance; and

- Limits on withdrawals to periods of recession or emergency, and to no more than two-thirds of the total balance in the first withdrawal year.

Download Executive Summary

Executive Summary: To Weather a StormA Rainy Day Fund is Desirable

Like most state and local governments New York City periodically faces fiscal hardships due to recessions. An RDF would provide stability by allowing New York City to smooth out spending during such contractions.

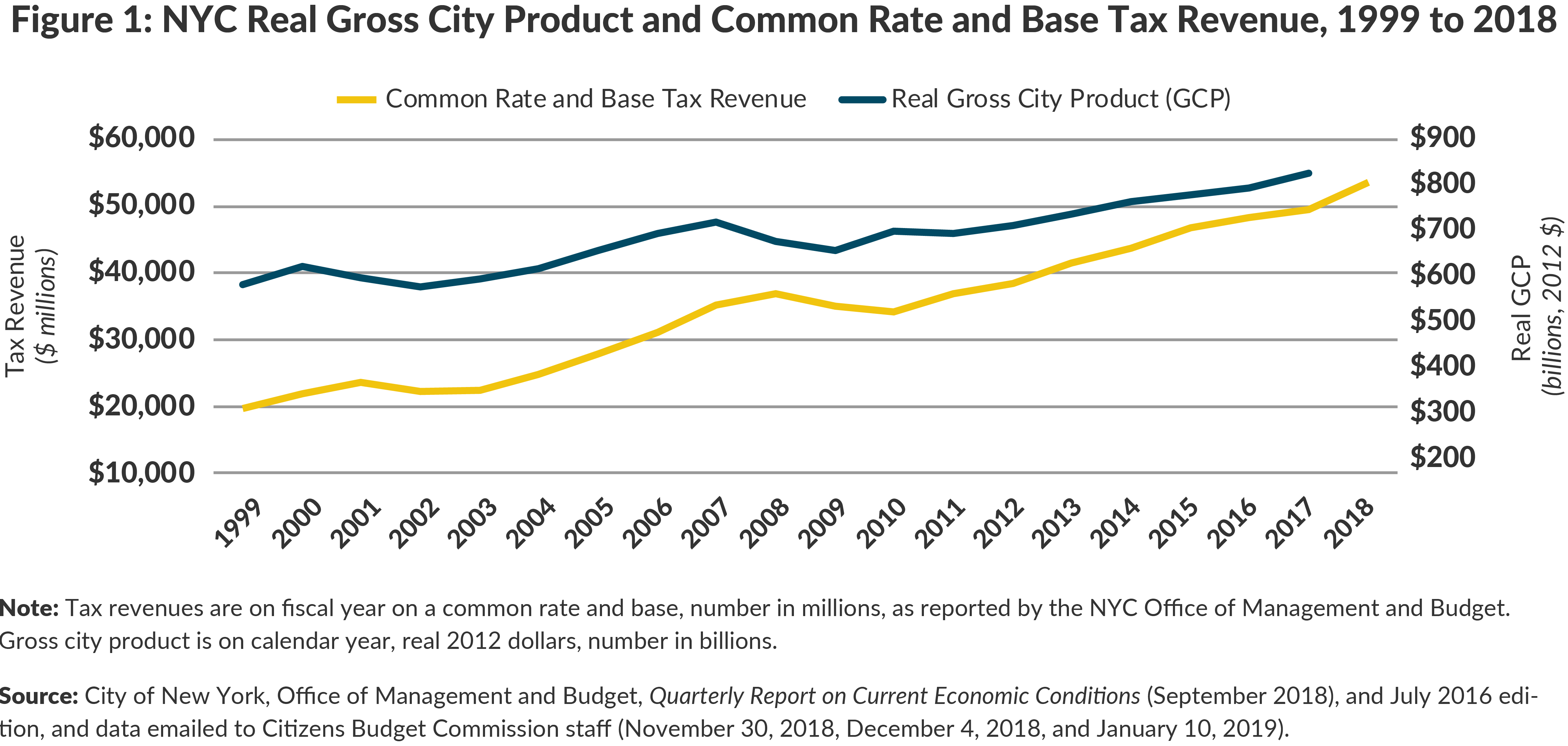

During the last two national recessions the city economy shrank; real dollar gross city product (GCP) fell 7.6 percent from calendar year 2000 to 2002 and did not return to pre-recession size until 2005, and it fell 9.0 percent from 2007 to 2009 and did not return to pre-recession size until 2013. (See Figure 1.)

The economic contractions caused tax revenues to decline. Tax revenues, adjusted for changes in tax law known as “common rate and base,” declined 5.4 percent and 5.5 percent in the first year following the 2001 and 2008 recessions, respectively. The second year after the 2001 recession saw sluggish growth of 0.5 percent, while the second year after the 2008 recession saw continued revenue declines of 2.4 percent.1 Since the City’s financial plans for those years assumed revenue growth, the tax losses generated even larger budget gaps.2

Absent sufficient reserve funds to offset the recession-related tax losses, New York, like other cities, faces painful choices. The federal government may enact counter-recessionary measures that include more intergovernmental aid to cities, but this often is insufficient to significantly ameliorate revenue losses and is counteracted by simultaneous cuts in state aid due to state revenue losses. In these circumstances a city must implement expenditure cuts, raise taxes, or imprudently rely on short-term borrowing to cover operating expenses. Each of these options is less desirable than being able to draw upon an RDF. Expenditure cuts typically lead to service reductions at a time when needs may increase; new taxes impose costs on residents and businesses at a time of economic difficulty and may lower a city’s competitiveness. Borrowing short-term generally is impractical because sufficient revenue may not be available to repay the debt within a fiscal year.

Although New York City has developed mechanisms to accumulate reserves absent an RDF (described below), these resources have been insufficient to weather recessions, and the City has had to turn to less desirable options. A substantial RDF would reduce the need for these actions. In the 2001-2003 recession, which began shortly before the terrorist attacks of 9/11, the City raised property taxes significantly, implemented a surcharge on personal income taxes, reduced services and the City workforce by 6,000, and borrowed about $2 billion in operating expenses related to the terrorist attack.3 Service cuts included suspending metal, glass, and plastic recycling, reducing the uniformed police force, closing fire companies, and reducing funding for libraries. 4 In the 2008-2010 recession the City rescinded a property tax rate reduction passed the prior year, raised the local sales tax by 0.5 percentage points, and reduced services, including cuts to summer youth programs and ambulance services, and a 14,000 headcount reduction in the municipal workforce.5

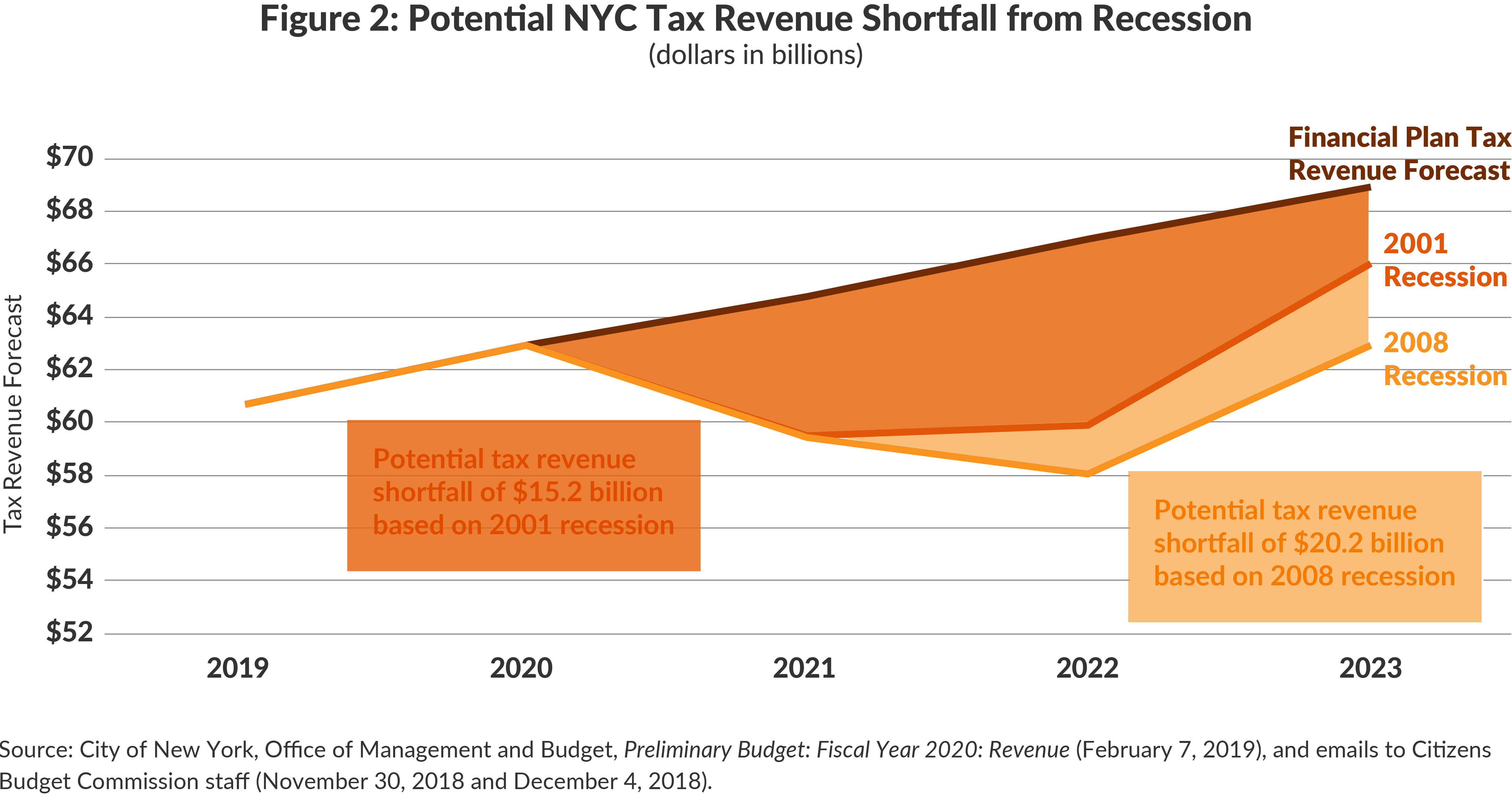

A recent Citizens Budget Commission (CBC) analysis estimated that a recession comparable to the last two recessions would result in cumulative tax revenue shortfalls of $15 billion to $20 billion over three years, compared to the current financial plan. (See Figure 2.)

Legal Constraints to New York City’s Use of a Rainy Day Fund

The City of New York is effectively precluded from having an RDF by provisions of State law and the City Charter. As a consequence of the City’s 1975 fiscal crisis, the State enacted the Financial Emergency Act for the City of New York (FEA). The statutory requirements have had beneficial effects helping local officials greatly improve the City’s fiscal management and health; they were incorporated in the City Charter in 2005.

However, the requirement that the City prepare a balanced budget and achieve balance in year-end results in accordance with generally accepted accounting principles (GAAP), included in both the FEA and the City Charter, has precluded the creation of an RDF. GAAP balance requires that revenues must be at least equal to expenditures in the City’s General Fund each year. Resources drawn from an RDF comprised of previously received funds would not count toward revenues in the year the draw is made because they would have been recorded as revenue in earlier years; they can only be counted as revenue once. Thus, while RDF funds would provide resources to fund current expenditures, there would be an imbalance between revenues and expenditures on a GAAP basis, which the FEA and City Charter preclude. Hence funding expenditures with RDF resources would still create a GAAP deficit and put the City in violation of State law and the City Charter.

Under the FEA as originally enacted, a deficit greater than $100 million would trigger a State Financial Control Board (FCB) control period, which would include a loss of local autonomy and accountability to the public, for which no mayor would want to be responsible. While an amendment to the FEA eliminated the automatic imposition of a control period, legislative action could reinstate the FCB’s ability to impose one in the event of a deficit.6 Furthermore, the City faces a substantial reputational risk—with bondholders, rating agencies, fiscal monitors, and the public—if it were to run a deficit.

Rainy Day Funds in Other Jurisdictions

Rainy Day Funds are common among the states—48 of the 50 states have them—though the effectiveness varies in part due to how the funds are structured. Among cities such funds are less common but are recognized as good fiscal management. Well-designed RDFs may assist credit ratings.[7]

Nonetheless, more than a dozen U.S. cities have RDF requirements in City Charter or local laws. Seattle, for example, established a Revenue Stabilization Fund with a target balance of 5 percent of tax revenue and statutorily required deposits.[8] Other cities, such as Cincinnati and Houston require that a minimum level of reserves be set aside but do not require minimum annual deposits.[9]

However, given the size of the City’s budget, the range of services it delivers, and the diversity of its tax base, RDF procedures and best practices for states serve as more appropriate guides than local practices. The Pew Charitable Trusts series on state RDFs recommend that target size be set based on historical revenue volatility, that deposits be based on a percentage of annual revenue growth in excess of typical levels, and that withdrawals be based on measurable conditions.[10] These best practices have guided the recommendations in this report.

New York City’s Rainy Day Fund Alternatives

Absent an RDF, New York City officials currently use three alternative mechanisms to set aside resources for use in troubled times: (1) annual budget reserves, (2) a “surplus roll,” and (3) reduced deposits to the Retiree Health Benefits Trust (RHBT) fund.

Annual Budget Reserves

In recent years the New York City budget has included appropriations for two budget reserves–the General Reserve and the Capital Stabilization Reserve. However, these are not available to be spent beyond the fiscal year in which they are established for the reasons described above.

The State law mandating the City’s balanced budget also requires that the budget include as an expenditure item a General Reserve of least $100 million; in recent years the Adopted Budget prudently has included a General Reserve greater than the minimum, often reaching or exceeding $1 billion. The General Reserve is essentially a contingency fund in the City’s operating budget: a line against which no specific expenditures have been programmed. During the course of the fiscal year, the General Reserve is eliminated gradually, with the funds shifted to pay for unanticipated spending or becoming part of the surplus roll, discussed below.

Beginning in fiscal year 2016 at the initiative of Mayor Bill de Blasio, the budget has also included a Capital Stabilization Reserve of $250 million.11 The purpose of the Capital Stabilization Reserve is to fund early stage capital project planning and design costs which do not qualify as capital investments eligible for funding from long-term borrowing, and to offset debt service costs due to rising interest rates. The Capital Stabilization Reserve generally has not been used and has been effectively available as a general reserve.

Surplus Roll

The surplus roll is the term for a group of expenditures made at the end of the fiscal year to effectively transfer resources from one fiscal year to the next in compliance with GAAP. Unused resources that accumulate during a fiscal year are used to “prepay” items which otherwise would be paid for in the following year, essentially “rolling” resources across fiscal years. The penalties for incurring a deficit have led City officials to budget cautiously and accrue unused resources over the fiscal year that would be a substantial year-end surplus. The sources of the surplus are higher than expected revenues and lower than planned spending.12

Surplus funds are used to prepay General Obligation (GO) and Transitional Finance Authority debt service, retiree health benefits costs, and subsidies to other legally distinct entities. These entities typically include NYC Health + Hospitals, the Metropolitan Transportation Authority, and the public library systems. The prepayments shift resources across fiscal years by paying next year’s expenses in the current year, thereby reducing expenditure in the upcoming fiscal year. This type of transaction is permissible under GAAP and serves to keep most of the surplus funds available for future operating expenses.

The surplus roll has two components: From the point of view of the current fiscal year, the “roll in” is the amount transferred in from the previous fiscal year, and the “roll out” is the amount transferred out to the subsequent fiscal year. When the roll out is larger than the roll in, the given fiscal year essentially ran an operating surplus, with current expenditures lower than current revenues. Conversely, when the roll in is larger than the roll out, the given fiscal year essentially ran an operating deficit, with current expenditures higher than current revenues.

Retiree Health Benefits Trust

The RHBT was created in fiscal year 2006 to accumulate resources to help pay for the future costs of health insurance and other benefits for retirees, referred to as other postemployment benefits (OPEB). The RHBT was a promising response to Government Accounting Standards Board (GASB) rules that require governments to report the cost of commitments to pay for retirees’ health benefits; New York City’s initial estimate in fiscal year 2006 was an unfunded liability of $54 billion. The initial RHBT deposit in 2006 of $1 billion was a start toward funding that obligation, and subsequent deposits in fiscal years 2007 and 2008 brought the balance to nearly $2.7 billion. However during the subsequent recession the City used the RHBT as a de facto rainy day fund; between fiscal years 2009 to 2013 about $2 billion was, in effect, diverted from deposits to the RHBT to pay for other City operating expenses.13 Beginning in fiscal year 2014, the City resumed making annual deposits. At the end of fiscal year 2018, the RHBT balance was $4.5 billion toward a liability that had grown to more than $103 billion.14

New York City’s RDF Alternatives Are Deficient

These RDF alternatives have three key deficiencies: 1) the reserves and surplus roll are not large enough, 2) increases and decreases to the surplus roll are discretionary and not tied to the economy, and 3) use of the RHBT as a de facto rainy day fund is fiscally imprudent.

Budget Reserves and Surplus Roll Are Not Large Enough

The combined resources of the General Reserve and Capital Stabilization Reserve are substantial and provide a significant cushion in the annual budget. However the total, although reaching $1.25 billion annually, is well below what is needed to significantly mitigate revenue losses during a recession, and those reserves would not be available for use in a future fiscal year. The $1.25 billion pales in comparison to the potential three-year tax revenue decline during a recession—$15 billion to $20 billion—with tax revenue potentially $5.3 billion below the financial plan in the first year and between $7 billion and $9 billion below the financial plan the following year. (See Figure 2.)

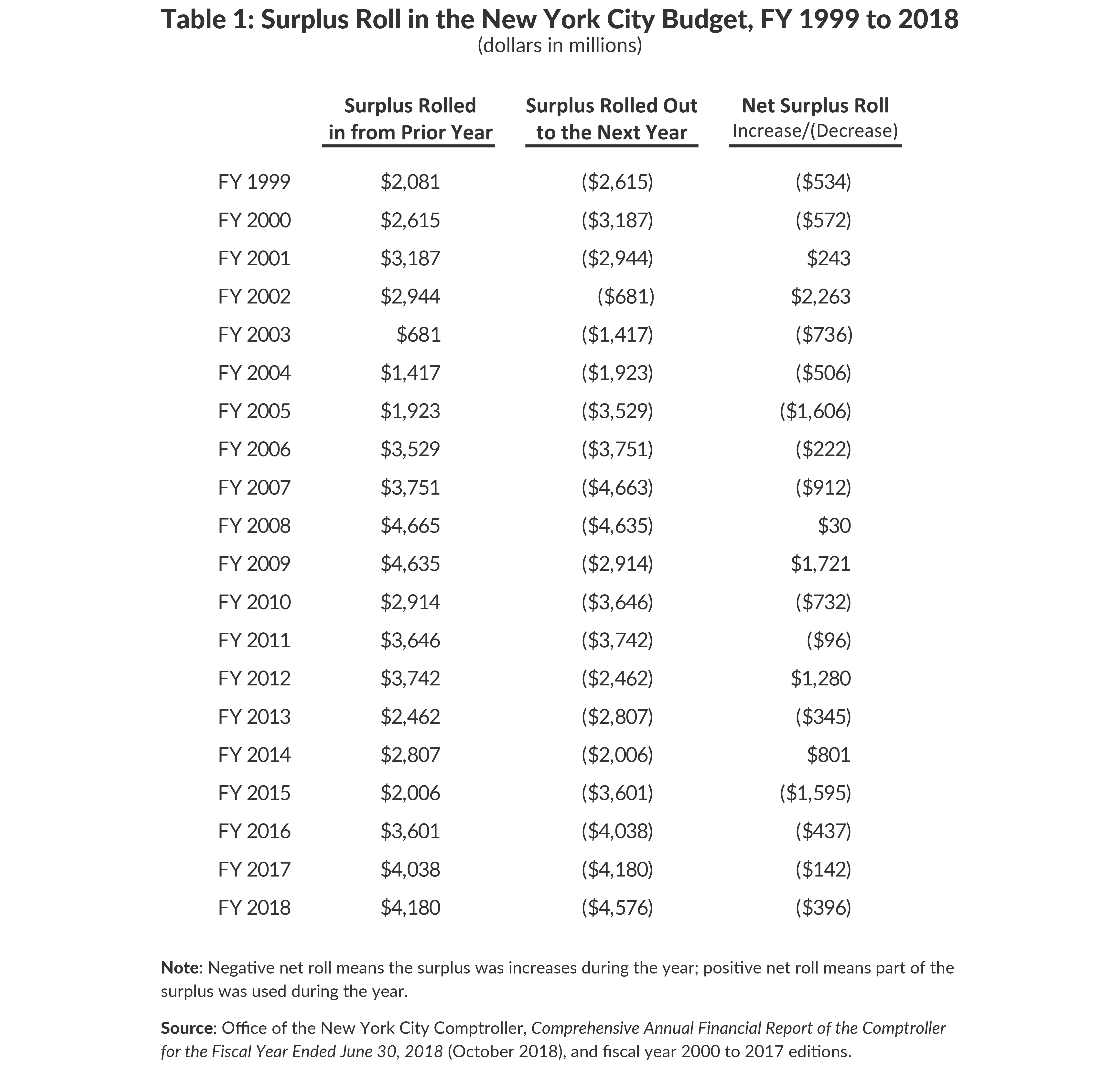

Even if reserves were large enough, the City cannot roll sufficient funds to substitute for an RDF. Since fiscal year 1999, the surplus roll exceeded $4.0 billion in four years and was as high as $4.7 billion.15 (See Table 1.) Limits to the expenses that can be prepaid at the end of the fiscal year constrains the surplus roll. For example, debt service totals $6.7 billion in fiscal year 2019; however, prepaying too much debt service would limit the City’s ability to levy property tax revenue due to the operating limit.16 Additionally, the subsidies that the City is able to prepay are limited; most of the City’s expenditures, such as salaries, wages, and contract payments, cannot be prepaid. Furthermore, there is concern that some stakeholders view the roll as a surplus that the City could spend, which could be used to justify calls for additional spending on services, labor contracts, and reductions in State support for City programs.

Additions and Subtractions to the Surplus Roll are Discretionary and Not Tied Directly to the Economy

The amount of the surplus roll in and surplus roll out each year are determined by the Mayor and the City Council. As a result, surplus roll resources can increase or decrease without regard to economic performance. Table 1 shows the roll in and out from fiscal years 1999 through 2018; for example, in fiscal year 2017, the City rolled in $4.038 billion in resources from fiscal year 2016 and then prepaid $4.180 billion of fiscal year 2018 expenses, essentially rolling that amount into the following year. While the City has added to the roll in most non-recession years, the size of the additions has varied in ways unrelated to patterns of economic growth; more importantly, the City used a portion of the surplus roll in fiscal years 2012 and 2014, when the City was not experiencing a recession.

Imprudent Use of the Retiree Health Benefits Trust

The Mayor and the City Comptroller view the RHBT as a potential source of reserves during a recession. However, this is an inappropriate use of the RHBT.17 The fund should accrue resources to pay for future OPEB obligations rather than requiring future generations to pay for retirement benefits promised to current workers providing current services.18 Diverting funds in the RHBT to pay for services during a recession in effect penalizes future generations in order to protect current residents.

Recommended Rainy Day Fund Design

To fund adequately and use appropriately an RDF, the enabling legislation should specify the target size, required deposits, and permitted withdrawals. A well-designed RDF is superior to the current mechanisms because it would require minimum deposits to build up resources during a recovery and permit withdrawals only during a recession or significant emergency. Additionally, the language should comport with GASB standards for restricted fund balances for stabilization arrangements, which includes specific criteria for when funds can be used.19 Lastly, changes to the FEA and the City Charter are necessary.

Target Size

The target size should be attainable and sufficient to mitigate most disruptive service cuts and counterproductive tax increases. Having an RDF to cover all gaps driven by a recession would present significant challenges to ongoing operating budgets. Though the effects of a recession can last into the third or even fourth year, designing the RDF to accumulate sufficient funds to ameliorate the most drastic negative effects in the first two years is reasonable.

Based on prior recessions, an RDF of 17.2 percent of pre-recession tax revenue would be appropriate. This estimate is based on the 2001 recession when the tax revenue declines from the pre-recession baseline year (fiscal year 2001) were 5.4 percent in the first year and 4.8 percent in the second year.20 While ideally funds would be available to support planned spending, resource constraints would be substantial and would make any spending growth challenging. However, given the City’s budget obligations, contractual wage agreements, and greater need for services during economic contraction, the RDF should provide funds to permit a constrained level of spending growth. From fiscal year 2000 to 2018, City-funded spending grew an average of 5.3 percent each year; the RDF should target funds to provide for annual spending growth of 2 percent. The 17.2 percent recommended size is also in line with the Government Finance Officers Association (GFOA) recommendation that municipalities keep reserves equal to at least two months of spending or 16.7 percent of expenditures.21

The absolute size of the RDF will increase over time as tax revenues increase during periods of economic growth. Applied to tax revenue projections for fiscal year 2020, the recommended size of the RDF would be $10.8 billion, rising to $11.9 billion in fiscal year 2023 under current tax revenue projections.

Required Deposits

In order to fund an RDF of this size, deposits should be required during periods of economic growth. Since December 1982, economic expansions have averaged six years; reaching 17.2 percent of revenue over six years would imply annual deposits of roughly 2.87 percent of tax revenue ($1.8 billion this year).22

However, such a deposit would be disruptive fiscally and would not reflect volatility in tax revenues. In light of this challenge, a practical approach is to require a mandatory minimum deposit of 75 percent of the tax revenue growth in excess of 3 percent annually. This minimum required deposit has two strengths. First, it leverages strong growth years by requiring larger deposits in years with high tax revenue growth and smaller (or no) deposits when tax revenue growth is more modest. Second, by excluding the first 3 percent of annual growth from deposits, it does not impede the City from having sufficient revenue growth to fund basic services, while prudently saving much of the elevated growth. For reference, common rate and base tax revenue grew an average 5.1 percent each year since fiscal year 2000, while inflation, measured by the Consumer Price Index averaged 2.3 percent each year from calendar year 2000 to 2018.23

Once the RDF reaches the target size, subsequent required deposits should be the amount needed to keep the RDF at 17.2 percent of tax revenues, up to the minimum required deposit.

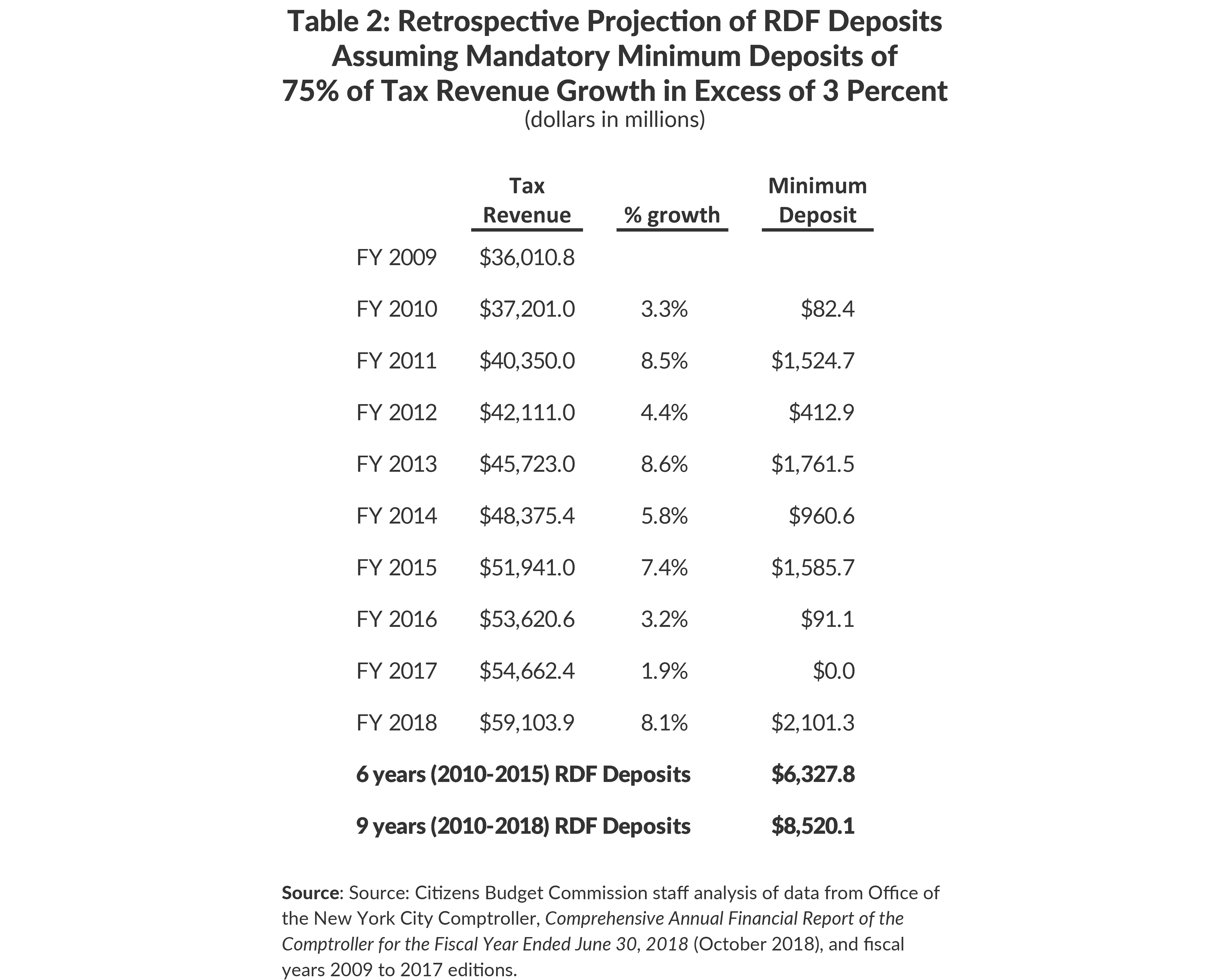

Based on actual tax revenue collections, the minimum deposits that would have been required in fiscal years 2010 through 2018 are shown in Table 2. Over the first six years, the average timeframe for a recovery, the RDF would have accumulated $6.3 billion, or 57 percent of the target balance.24 Over the current exceptionally long nine-year expansion, the RDF would have built up $8.5 billion, or 76 percent of the target balance. While these amounts do not meet the target, they would be a significant improvement over the current level of reserves.

The recommended deposit rule is a minimum that balances setting aside substantial resources with being fiscally manageable. However, as the data show, minimum deposits would not generate the level of reserves the City should aim to set aside; deposits in excess of the minimum should be encouraged, especially in years of substantial revenue growth when unexpected, one-time revenues are generated. For example, the deposit rules for California’s Budget Stabilization Account require that, in addition to 1.5 percent of general fund revenues, the State deposit an amount equal to taxes on capital gains exceeding a certain level, capturing this volatile revenue source in years when it is high.25

The budget and all financial plan updates should include an appropriation for the projected RDF deposit based on the tax revenue forecast and should be updated throughout the fiscal year. Upon release of the Comprehensive Annual Financial Report (CAFR), the New York City Comptroller should be required to certify the required RDF deposit for the preceding fiscal year based on final audited tax revenue figures. Any shortfall between the certified required deposit and the amount deposited the previous fiscal year should be appropriated in the current year.26 The deposit would be credited back to the prior year and would not reduce the required deposits in that year.

Permitted Withdrawals

The third design element of an RDF is to limit withdrawals to ensure the RDF is used at appropriate times and not depleted in one year. There are two situations under which a withdrawal could be initiated:

- An economic contraction defined as two quarters of declining real GCP; or

- A severe emergency, such as a natural disaster or terrorist attack, accompanied by significant, unanticipated revenue loss or expenditure needs.27

Withdrawals would need to commence within 12 months of the triggering event and could continue until tax revenues exceed pre-contraction levels on a common rate and base as measured by the New York City Office of Management and Budget (OMB).

City officials should not be able to draw on the RDF when common rate and base tax revenues are growing or when tax revenues decline due to policy changes, based on common rate and base tax data maintained by OMB. Furthermore, withdrawals should be limited so that the entire RDF is not depleted in a single year. A reasonable limit on withdrawals is no more than two-thirds of the balance in the first fiscal year the fund is used.

Required City Charter and State Law Changes

Current City and State requirements for balanced budgets using GAAP preclude the City from creating and using an RDF. The City Charter and the FEA would have to be amended to enable an RDF.28

Precedent exists for modifying the legal requirement of adherence to GAAP. A deviation from GAAP was enacted after GASB issued a rule, effective fiscal year 2009, that required pollution remediation expenses including those for asbestos removal be treated as operating expenses rather than capital investments. The FCB initially granted the City a two-year deferral of the requirement; in 2011 the City sought and obtained a permanent exemption.29 The State legislature amended the FEA to deem these pollution remediation expenses as capital and superseded the City Charter requirement for a GAAP balanced budget and actuals.30

State law and City Charter changes would require two parts. One is for the State and City to adopt laws establishing the RDF. This language would codify the target size, deposit requirements, permitted withdrawals, and maximum withdrawal levels. The other is to amend the FEA and City Charter to permit the RDF to be used. Two potential approaches to amending Section 8(1)(a) of the FEA are:

Immediate Benefits

The current expansion is in its ninth year, and it is extremely unlikely that a newly established RDF would accumulate sufficient resources before the next recession. Nevertheless, creating one at this time would be beneficial both in the short and long term. Any resources that the City is able to set aside in an RDF prior to the next recession would reduce the need to cut services and enact counterproductive tax increases. More importantly, having the legal framework in place when the next expansion begins would allow the City to make deposits as soon as tax revenue growth recovers sufficiently.

Conclusion

New York City requires a substantial RDF in order to weather future recessions without harmful service cuts or counterproductive tax increases. The key elements for such an RDF are adequate balances, required deposits, and limits on withdrawals. Establishing such a fund requires changes to the City Charter and State statute. Such changes could be made in a way that would not undercut the beneficial legal requirements for sound budgeting that have served the City well since the 1970s fiscal crisis. Creating and funding an RDF will require fiscal discipline to allocate the needed funds from the City’s operating budget but will benefit New Yorkers by helping the City provide needed services in good times and bad.

City leaders should address these challenges and commit to establishing a meaningful RDF in order to secure the City’s long-term fiscal future in the face of economic uncertainty. The State should support the City’s effort to maintain responsible fiscal management and prepare for economic downturns by facilitating statutory change in the FEA and viewing the RDF as an important fiscal tool for the City rather than as a resource justifying reductions in State assistance.

Download Report

To Weather a Storm: Create an NYC Rainy Day FundFootnotes

- City of New York, Office of Management and Budget, Common Rate and Base Tax Revenue from 1999 to 2018, emails to Citizens Budget Commission staff (November 30, 2018 and December 4, 2018).

- Michael Dardia and Rachel Bardin, “How Much to Bank on? When it Comes to Revenue Forecasting, Better Safe Than Sorry,” Citizens Budget Commission Blog (April 12, 2015), https://cbcny.org/research/how-much-bank-when-it-comes-revenue-forecasting-better-safe-sorry.

- It is unlikely that this borrowing would have been approved due to the 2001 recession alone; the terrorist attack of September 11, 2001 had substantial negative impacts on New York City and its economy that called for unprecedented response. The long-term borrowing for operations was authorized by the State through the enabling legislation for the Transitional Finance Authority that issued the bonds; currently, long-term borrowing for operations is not permitted by the Financial Emergency Act for the City of New York or the City Charter. Douglas Offerman and Marcia Van Wagner, The City’s Budget Gap Since 9/11: Factors That Cause It, and Plans to Close It (Citizens Budget Commission, March 3, 2003), https://cbcny.org/research/citys-budget-gap-911.

- City of New York, Office of Management and Budget, Financial Plan for Fiscal Years 2002-2006: Summary Book (February 13, 2002), www1.nyc.gov/assets/omb/downloads/pdf/sum1_02.pdf, and November 2002 Financial Plan: Fiscal Years 2003-2006: Summary (November 14, 2002), www1.nyc.gov/assets/omb/downloads/pdf/sum11_02.pdf.

- City of New York, Office of Management and Budget, November 2009 Plan: Budget Summary (November 5, 2008), www1.nyc.gov/assets/omb/downloads/pdf/fp11_08.pdf, January 2009 Financial Plan: Fiscal Years 2009-2013 (January 30, 2009), www1.nyc.gov/assets/omb/downloads/pdf/tech1_09.pdf, and Financial Plan Summary: Fiscal Years 2009-2013 (May 1, 2009), www1.nyc.gov/assets/omb/downloads/pdf/sum5_09.pdf.

- The FEA provision defining a control period includes language that a control period cannot extend beyond July 1, 2008; however, the FCB could ask the State to impose a control period in the case of a deficit. Section 2(12) of the New York State Senate, New York State Financial Emergency Act for the City of New York 868/75, Unconsolidated Laws of New York (accessed April 15, 2019), www.nysenate.gov/legislation/laws/FEA/2.

- The Pew Charitable Trusts, Rainy Day Funds and State Credit Ratings: How well-designed policies and timely use can protect against downgrades (May 18, 2017), www.pewtrusts.org/en/research-and-analysis/reports/2017/05/rainy-day-funds-and-state-credit-ratings.

- City of Seattle, Charter of the City of Seattle, Title 5, Subtitle III – Funds, Chapter 5.80 Cumulative Reserve Funds (accessed April 3, 2019), https://library.municode.com/wa/seattle/codes/municipal_code?nodeId=TIT5REFITA_SUBTITLE_IIIFU_CH5.80CUREFU_5.80.020RESTFU.

- City of Cincinnati, Ordinance 253-2015 (accessed April 3, 2019), http://city-egov.cincinnati-oh.gov/Webtop/ws/council/public/child/Blob/43054.pdf?rpp=-10&m=2&w=doc_no%3D%27201501014%27; and City of Houston, Adopted Operating Budget for the Period July 1, 2018 to June 30, 2019, pp. I-14 – I-20, https://www.houstontx.gov/budget/19budadopt/FY2019_Adopted_Budget.pdf.

- The Pew Charitable Trusts, Fact Sheet: Rainy Day Fund Best Practices: Guidelines for deposits, withdrawals, and size (April 10, 2017), www.pewtrusts.org/en/research-and-analysis/fact-sheets/2017/04/rainy-day-fund-best-practices.

- In the Adopted Fiscal Year 2016 Budget, the Capital Stabilization Reserve was $500 million for fiscal year 2016. This was replicated in the Adopted Fiscal Year 2017 Budget, with a $500 million reserve for fiscal year 2017. Beginning with the Preliminary Fiscal Year 2018 Budget, the Capital Stabilization Reserve has been $250 million per year in each of the financial plan years.

- The sources of the surplus include low estimates of revenues, high assumptions about interest rates and volume of borrowing that yields lower debt service expenditures, high assumptions about increases in health insurance premiums for employees and retirees, current year savings from Programs to Eliminate the Gap or Citywide Savings Programs, agency underspending, unused resources in the budget reserves, and recognition of obligation booked in prior years that are being paid in the current year. The City recognizes a negative value for prior year payables in the current year, generally mid-year, which reflects expenditures being made during the year that were already booked in prior years, freeing up around $400 million in current year resources annually.

- Office of the New York City Comptroller, Measuring New York City’s Budgetary Cushion: How Much is Needed to Weather the Next Fiscal Storm? (August 4, 2015), https://comptroller.nyc.gov/reports/measuring-new-york-citys-budgetary-cushion-how-much-is-needed-to-weather-the-next-fiscal-storm/; and Thad Calabrese, The Price of Promises Made: What New York City Should Do About Its $95 Billion OPEB Debt (Citizens Budget Commission, October 25, 2017), https://cbcny.org/research/price-promises-made.

- The Comprehensive Annual Financial Report for the City reported the balance at the end of fiscal year 2018 as $4.8 billion, which included a $300 million prepayment of fiscal year 2019 retiree health and welfare costs that have been netted out. Office of the New York City Comptroller, Comprehensive Annual Financial Report for the Fiscal Year Ended June 30, 2018 (October 31, 2018), https://comptroller.nyc.gov/wp-content/uploads/documents/CAFR2018.pdf.

- Table 1 reports only the surplus roll into and out of each year. In some years the City also deposits funds in the RHBT or defeases long-term debt. For example, in fiscal year 2007, in addition to rolling $4.7 billion into fiscal year 2008, the City deposited $1.5 billion in the RHBT and defeased $1.3 billion in debt. The total surplus, including these two discretionary actions was $7.5 billion.

- The primary prepayment is debt service, which can cause the City to approach the operating limit for property tax. The City is authorized to levy a property tax to pay long-term debt service; the property tax levy for operating expenses is subject to the operating limit of 2.5 percent of the five-year average market value. Prepaying substantial GO debt service reduces the amount of the property tax that is used for debt service and increases the amount used for operating expenses, which can bring the City close to the operating limit; in fiscal years 2006, 2007, 2016, 2017, and 2018, the City used more than 98 percent of the operating limit. City of New York, Department of Finance, Annual Report of the New York City Property Tax: Fiscal Year 2018 (April 2018), p. 53, www1.nyc.gov/assets/finance/downloads/pdf/reports/reports-property-tax/nyc_property_fy18.pdf.

- Contributions to and use of funds within the RHBT have been consistent with the legal requirements set in Local Law 19 of 2006, https://legistar.council.nyc.gov/View.ashx?M=F&ID=667718&GUID=BE279B59-AD32-417B-8366-4CE35A57838B.

- CBC recommends the City Charter be amended to mandate the RHBT, require annual deposits, and limit disbursements to the current year cost of retiree health and welfare benefits. Testimony of Andrew Rein, President, Citizens Budget Commission, before the 2019 Charter Revision Commission (March 11, 2019), https://cbcny.org/advocacy/testimony-charter-defined-budget-and-management-practices. Furthermore, CBC has recommended OPEB benefits be reduced to better align with the level of benefits provided by other municipalities while establishing appropriate funding arrangements. See: Thad Calabrese, The Price of Promises Made: What New York City Should Do About Its $95 Billion OPEB Debt (Citizens Budget Commission, October 25, 2017), https://cbcny.org/research/price-promises-made.

- GASB requires the “specific circumstances under which a need for stabilization arises” be identified and described, and that these “circumstances should be such that they would not be expected to occur routinely.” Government Accounting Standards Board, Statement No. 54 of the Governmental Accounting Standards Board: Fund Balance Reporting and Governmental Fund Type Definitions (February 2009), p. 9, https://gasb.org/resources/ccurl/313/494/GASBS%2054.pdf.

- For the 2008 recession, the comparable percentage declines are 5.5 percent and 7.8 percent. City of New York, Office of Management and Budget, Common Rate and Base Tax Revenue from 1999 to 2018, emails to Citizens Budget Commission staff (November 30, 2018 and December 4, 2018).

- Government Finance Officers Association, Fund Balance Guidelines for the General Fund (accessed March 28, 2019), www.gfoa.org/fund-balance-guidelines-general-fund.

- The average length of time between the last three recessions in New York State was 76 months. The expansion from December 1982 to March 1989 was 75 months, the expansion from November 1982 to December 2000 was 97 months, and the expansion from August 2003 to April 2008 was 56 months. State of New York, Department of Labor, Recessions in New York State (accessed April 3, 2019), www.labor.ny.gov/stats/recessions_nys.shtm.

- City of New York, Office of Management and Budget, Common Rate and Base Tax Revenue from 1999 to 2018, emails to Citizens Budget Commission staff (November 30, 2018 and December 4, 2018); and U.S. Department of Labor, Bureau of Labor Statistics, Consumer Price Index – New York-Newark-Jersey City, NY-NJ-PA (1982-84=100), All Urban Consumers (CPI-U) (accessed April 15, 2019), www.bls.gov/regions/new-york-new-jersey/data/xg-tables/ro2xgcpiny.htm.

- The funds in the RDF would earn interest which would contribute positively to the balance and are not reflected in Table 2. Assuming a conservative return of 1.3 percent per year, the average return earned on the City cash reserves in fiscal year 2018, the RDF could have earned $246 million over the first six years or $536 million over the nine-year period. Office of the New York City Comptroller, Comprehensive Annual Financial Report for the Fiscal Year Ended June 30, 2018 (October 31, 2018), https://comptroller.nyc.gov/wp-content/uploads/documents/CAFR2018.pdf.

- Mariana Alexander and Timothy Sullivan, California Dreaming: NY Should Build Reserves to Prepare for a Rainy Day (Citizens Budget Commission, March 12, 2018), https://cbcny.org/research/california-dreaming.

- The legislation could allow for deposits to be spread over two years if the shortfall exceeds a certain threshold.

- To comport with GASB 54, the circumstances should be those that are not expected to occur routinely. Furthermore, consideration should be given to codifying the definition of a natural disaster or emergency, including whether there needs to be an executive declaration of emergency. Government Accounting Standards Board, Statement No. 54 of the Governmental Accounting Standards Board: Fund Balance Reporting and Governmental Fund Type Definitions (February 2009), p. 9, https://gasb.org/resources/ccurl/313/494/GASBS%2054.pdf.

- Amending the City Charter is insufficient; the State FEA must be amended by the State legislature to permit the RDF. The City Charter can be amended through voter referendum or by the City Council; additionally, the State legislature can amend the Charter directly or can supersede the Charter, as was done when the GASB 49 exemption was added to the FEA.

- Office of the New York City Comptroller, Policies and Procedures Manual for the Implementation of Governmental Accounting Standards Board Statement No. 49 – Accounting and Financial Reporting for Pollution Remediation Obligations (version 2.0, May 2010), https://comptroller.nyc.gov/wp-content/uploads/2013/07/GASB-49-Policy-and-Procedure-Manual-revised.pdf.

- The relevant statutory language is, “Notwithstanding the foregoing and the provisions of any general or special state law or local law to the contrary, including but not limited to the New York City charter, all costs that would be capital costs in accordance with generally accepted accounting principles, but for the application of governmental accounting standards board statement number forty-nine, shall be deemed to be capital costs for the purposes of this chapter and any other provision of state or local law, including but not limited to the New York City charter, relevant to the treatment of such costs.” See: Section 8(1)(a) of the New York State Senate, New York State Financial Emergency Act for the City of New York 868/75, Unconsolidated Laws of New York (accessed April 15, 2019), www.nysenate.gov/legislation/laws/FEA/8; and Charles Brecher, What is a “Balanced Budget”? (Citizens Budget Commission, November 8, 2011), https://cbcny.org/research/what-balanced-budget.

- “The city’s budget covering all expenditures other than capital items shall be prepared and balanced so that the results thereof would not show a deficit when reported in accordance with generally accepted accounting principles.” Section 8(1)(a) of the New York State Senate, New York State Financial Emergency Act for the City of New York 868/75, Unconsolidated Laws of New York (accessed April 15, 2019), www.nysenate.gov/legislation/laws/FEA/8.